Key terms

Understanding a few key terms will make it easier to navigate what is sometimes a complex ETF process.

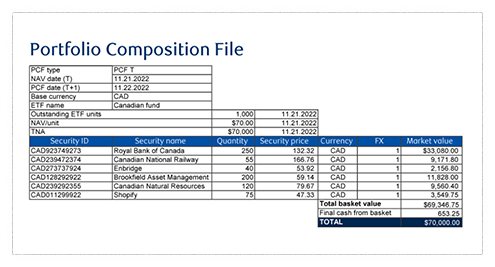

Figure 1

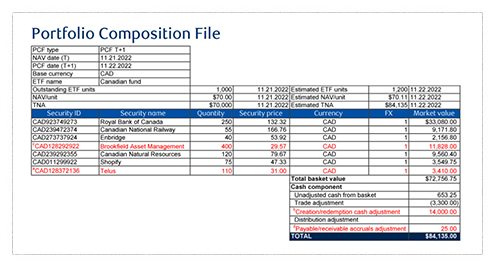

Figure 2

Figure 3

Understanding a few key terms will make it easier to navigate what is sometimes a complex ETF process.

Operating within the primary market, the authorized participant delivers a basket of underlying securities and/or cash (“creation basket”) to the ETF issuer in exchange for a block of units in the underlying ETF with the equivalent market value (“creation unit”). These units represent an inventory that can be bought and sold on the secondary market. Upon depleting their ETF units, the authorized participant repeats the creation process, delivering additional securities in exchange for new ETF units.

The authorized participant may also redeem ETF units by accumulating enough ETF shares to constitute at least a creation unit and then exchanging these ETF shares with the ETF issuer for an equivalent basket of underlying securities. This can occur if many ETF investors choose to sell their investments at the same time.

The make-up and construct of the securities that comprise an ETF creation basket are determined by the Portfolio Composition File (PCF), which:

The PCF reflects:

The accompanying simulated Canadian equity portfolio illustrates how the PCF is employed by the issuer to create a block of new ETF units (creation unit) for the authorized participant to sell in the secondary market.

The authorized participant is the entity approved by the issuer to create and redeem ETF units, providing transparency and liquidity to the market. Transparency and liquidity go hand in hand. Transparency refers to alignment of the ETF unit price with the respective NAV, while liquidity is the mechanism used to deliver this transparency.

Where demand for ETF units exceeds supply, the unit price rises above the NAV. To realign the price and satisfy excess demand, the authorized participant creates ETF units and issues them to the market. Conversely, when excess units are in circulation, the authorized participant redeems units to bring supply back into alignment with demand and the underlying NAV of the fund.

The partnership forged by the issuer, authorized participant and investor is beneficial to all three parties. There are often multiple authorized participants with bids and offers on an ETF. Each is looking for the opportunity to match buyers and sellers in the secondary market, and this competition drives more attractive bid and asking prices.

The asset servicing provider is central to the ETF creation and redemption process, working closely with the issuer and authorized participant to provide the following administrative services:

Transfer agency

Maintain records of the ETF creation and redemption activity

Global custody

Provide settlement, safekeeping, corporate actions and agent lending services

Fund accounting and administration

Calculate the Net Asset Value (generally shown as NAV/unit) and source the securities pricing

Order management

Facilitate the execution of trade orders

Portfolio composition file calculation

Maintain the current list of securities held within the ETF

Consulting

Offer ETF education, advice on product development and launches, and other consultative services

The asset servicing functions are generally delivered by a single provider as a “one-stop shop.” However, these functions may also be supplied by multiple providers.

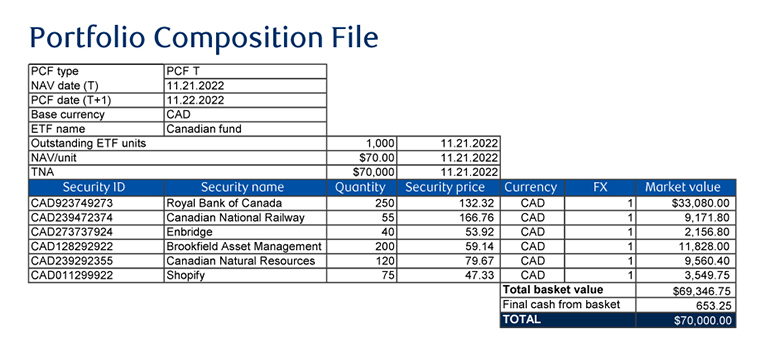

The PCF process starts by calculating the Total Net Assets (TNA) of the ETF at close of business on the NAV date. In this simulated Canadian portfolio (all currencies in CAD), the fund has a TNA of $70,000 at close of business on the NAV date (November 21, 2022), including 1,000 outstanding ETF units and a NAV of $70/unit as shown in Figure 1.

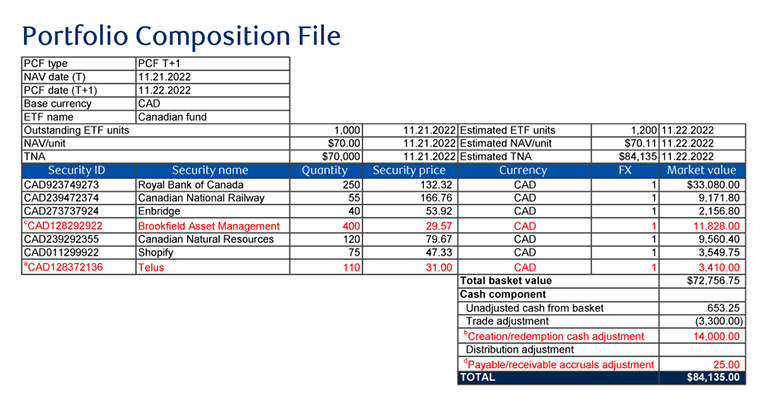

The objective of the PCF is to project the make-up of the fund at close of business on the next trading day following the NAV date (i.e., November 22, 2022) to let the authorized participant know what to deliver to the issuer in exchange for each creation unit. To come up with this end-of-day projection, it is necessary for the PCF to account for various intra-day activities. Figure 2 provides a view of where the fund will be at close of business on the next trading date following the NAV date, including the following intra-day activities, which are red highlighted:

| Intra-day activity | PCF updates, including impact on simulated portfolio (see Figure 2) | |

|---|---|---|

| a. Trades |

|

Investment manager trades: Buy 110 shares of Telus @ $30/share ($3,300) |

| b. Creations and redemptions |

|

Transfer agent activity: Next-day net creation of 200 ETF units @$70/unit in cash ($14,000) |

| c. Corporate actions |

|

Corporate actions activity: Brookfield Asset Management 2-for-1 split (additional 200 shares) |

| d. Fund distributions | Reflect ETF distributions in the cash component | Dividend ex. 11.22.2022: Royal Bank of Canada, 10ȼ/share ($25 receivable) |

Figure 2 represents the “total fund” and needs to be modelled to reflect the basket size based on the prescribed number of units (PNUs) for use by the authorized participant. It will be necessary to:

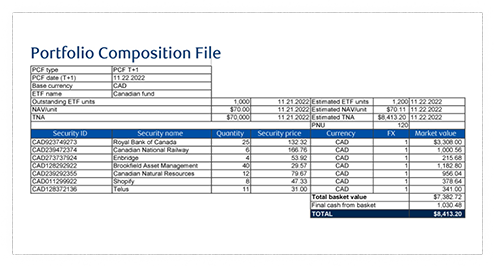

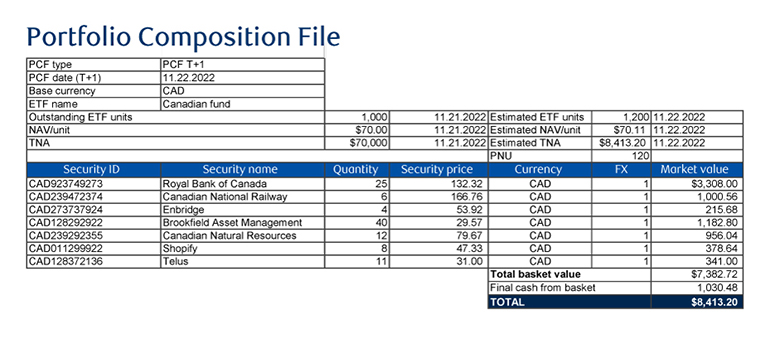

Figure 3 has been updated to reflect the basket size to be used by the authorized participant—a basket PNU of 120 units or 10% of the estimated ETF units. As a result, each security position in the creation basket equals 10% of the individual security positions, generating a basket component value of $7,382.72, as well as a final cash component of $1,030.48—the difference between the total value of the creation basket ($8,413.20) and the aggregate value of the security positions in the basket ($7,382.72).

Figure 3 shows that the authorized participant needs to deliver to the issuer by settlement date a basket of securities valued at $7,382.72 plus cash of $1,030.48 (creation basket totaling $8,413.20) in exchange for 120 ETF units (creation unit totaling $8,413.20). This is identical to what the authorized participant would receive in the form of securities and cash to redeem 120 ETF units.