Appointed subcustodians

Some markets are restricted for UCITS funds investment – please refer to your depositary team

Egypt

Updated as at December 30, 2022

Market Account Opening Requirements

FII Market Entry Requirements for Egypt RBC IS operates a segregated account structure in this market. Please refer to 'Market Account Opening Requirements' for information on the market requirements. Clients are requested to refer to the requirements for information purposes only. For further information or support around accessing this market, please contact your RBC IS representative. |

Market Statistics

| Currency | Egyptian Pound (EGP) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Time Zone | GMT + 2 (DST may apply) | ||||||||

| Egyptian Exchange (EGX) |

Figures as of June 2022 Source of information is available at: https://egx.com.eg/en/MarketIndicator.aspx |

Market Infrastructure

| Exchange(s) |

Egypt has one stock exchange with two locations, one based in Alexandria, and the main exchange in Cairo. The two exchanges locations are linked electronically and operate as a single market. Both are governed by the same chairman and board of directors and were referred to as the Cairo and Alexandria Stock Exchanges (CASE). The Alexandria Stock Exchange was officially established in 1888, followed by the Cairo Exchange in 1903. The two exchanges were very active in the 1940s and the Egyptian stock exchanges ranked fifth in the world. The market shrank dramatically after 1959, following a spate of restrictions and nationalisations. CASE is now formally known as The Egyptian Exchange (EGX) with effect from 21 July 2008 Launched in November 2007, the NILEX is a stock exchange dedicated to small to medium sized enterprises (SMEs) and currently has 32 listed companies with a trade settlement at T+2 basis.

Market Fees

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Trading System | The trading system at EGX has perceived gradual development from an outcry system (prior to 1992) to an automated order-driven system. As a result of the growth in business, the exchange got hold of a proven and scalable system conforming to international standards and up-to-date technology. |

||||||||||

| Trading Hours | Discovery Session*:- 9.30am ---9.50am - 10:00am (Random close) Official Trading Session:- 10 am----2.30 pm Bonds Market (Primary Dealers):- 10 am---2.30 pm NILEX (SMEs Market):- 10:00 am ------2.30 pm Block Trades:- 9.15 am-----9.45 am Omnibus Accounts:- 2.30 pm-----3.30 pm Over the counter market:Over-the-CounterMarket Deals Market--9.30 am---2 pm OTC Market (dematerialised securities):- 9.30 am---11 am Orders Market**12 pm--12.30 pm Effective 7/8/2014 trading session |

||||||||||

| Security Identifiers | ISIN (International Securities Identification Numbering): Yes |

||||||||||

| Regulatory Bodies | Ministry of Investment: oversees the Financial Regulatory Authority (FRA). It supports the government's mandate to implement reform programmes aimed at improving investments in different sectors, adopting the role of coordinator of institutions and ministries. The ministry implements the asset management programme. FRA reports directly to the prime minister with dotted line to the minister of investment. The Authority is responsible for supervising and regulating non-banking financial markets and instruments, including the Capital Market, Insurance Services, Mortgage Finance, Financial Leasing, Factoring and Securitization. FRA's role is to regulate the market and ensure its stability and competitiveness to attract more local and foreign investments. " The mandate of the Authority also includes limiting inconsistency risks and addressing problems arising from applying different supervisory rules". The Egyptian Financial Supervisory Authority is replacing the Egyptian Insurance Supervisory Authority, the Capital Market Authority, and the Mortgage Finance Authority in application of the provisions of the supervision and regulation of Insurance law no. 10 of 1981, the Capital Market law no. 95 of 1992, the Depository and Central registry law no. 93 of 2000, the Mortgage Finance law no. 148 of 2001, as well as other related laws and decrees that are part of the mandates of the above authorities. FRA is also the admin authority for companies established under the provisions of law of financial leasing issued by law no.95 for year 1995r 2009. The Central Bank of Egypt (CBE) is an autonomous regulatory body, assuming the authorities and powers vested therein by Law No. 88 for 2003, and the Presidential Decree No. 65 for 2004. The main objectives and functions of the CBE are as follows:- - Realizing price stability and ensuring the soundness of the banking system - Formulating and implementing the monetary, credit & banking policies - Issuing banknotes and determining their denominations and specifications - Supervising the banking sector - Managing the foreign currency international reserves of the country. - Regulating the functioning of the foreign exchange market. - Supervising the national payments' system. - Recording and following up on Egypt's external debt (public and private) Authorities and powers vested therein by Law No. 88 for 2003, and the Presidential Decree No. 65 for 2004. |

||||||||||

| Instruments |

|

||||||||||

| Form of Securities | Over 99.6% of the equities market is dematerialised |

||||||||||

| Board Lots | There are no set board lots. However, all Treasury-bill (T-bill) trades must have a nominal value of EGP 25,000 or its multiples. |

||||||||||

| Price Variations | Circuit breakers - price limit for temporary suspension is 10% with suspension time of 10 minutes. Price limit for suspension for the rest of the trading day is 20%. EGX can also adjust the temporary suspension time from 10-30 minutes at its own discretion, according to market conditions. EGX will still be able to resort to suspension in the case of sudden or unexpected changes in stock prices. |

Settlement & Registration

| Settlement Cycles |

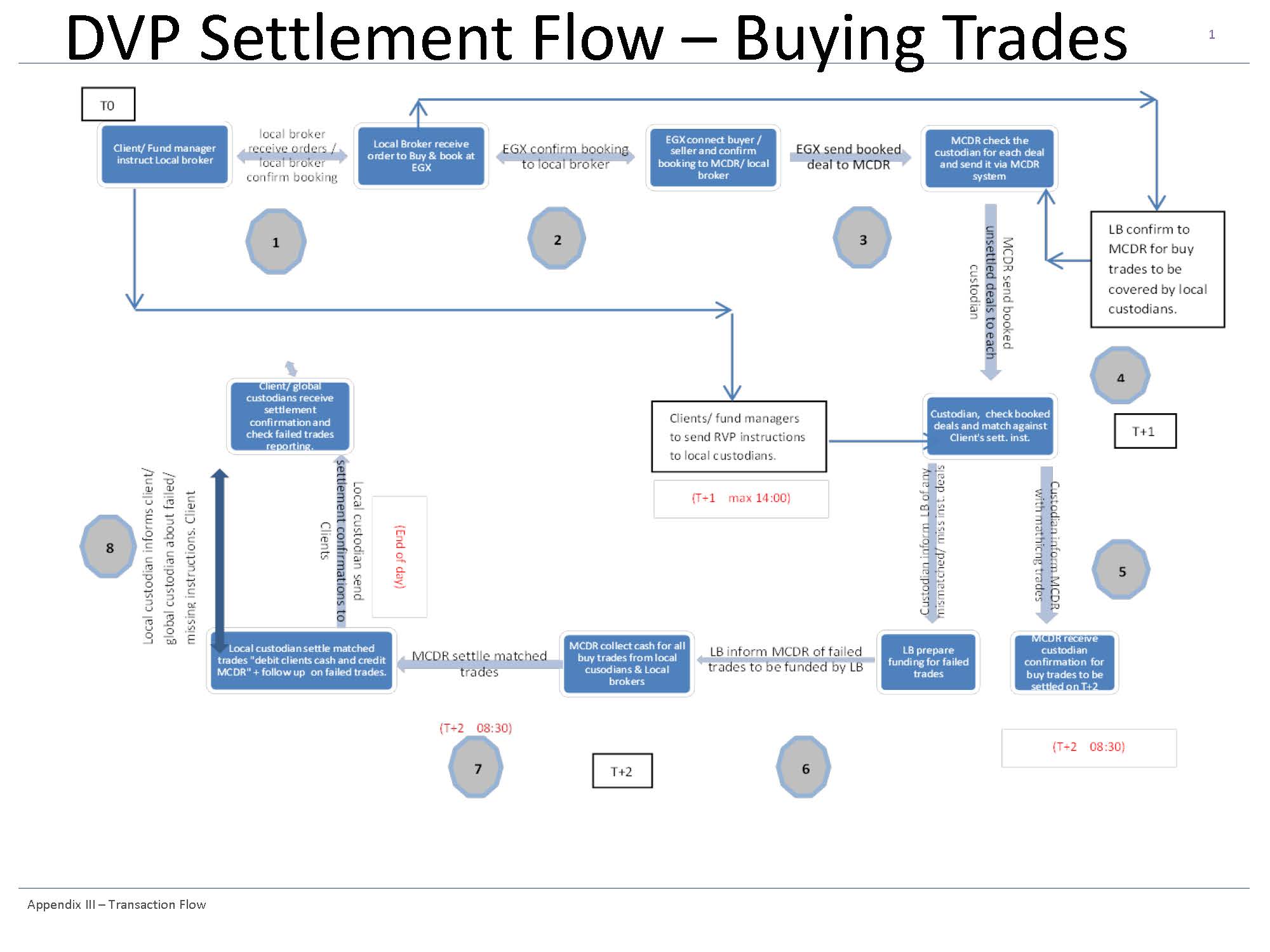

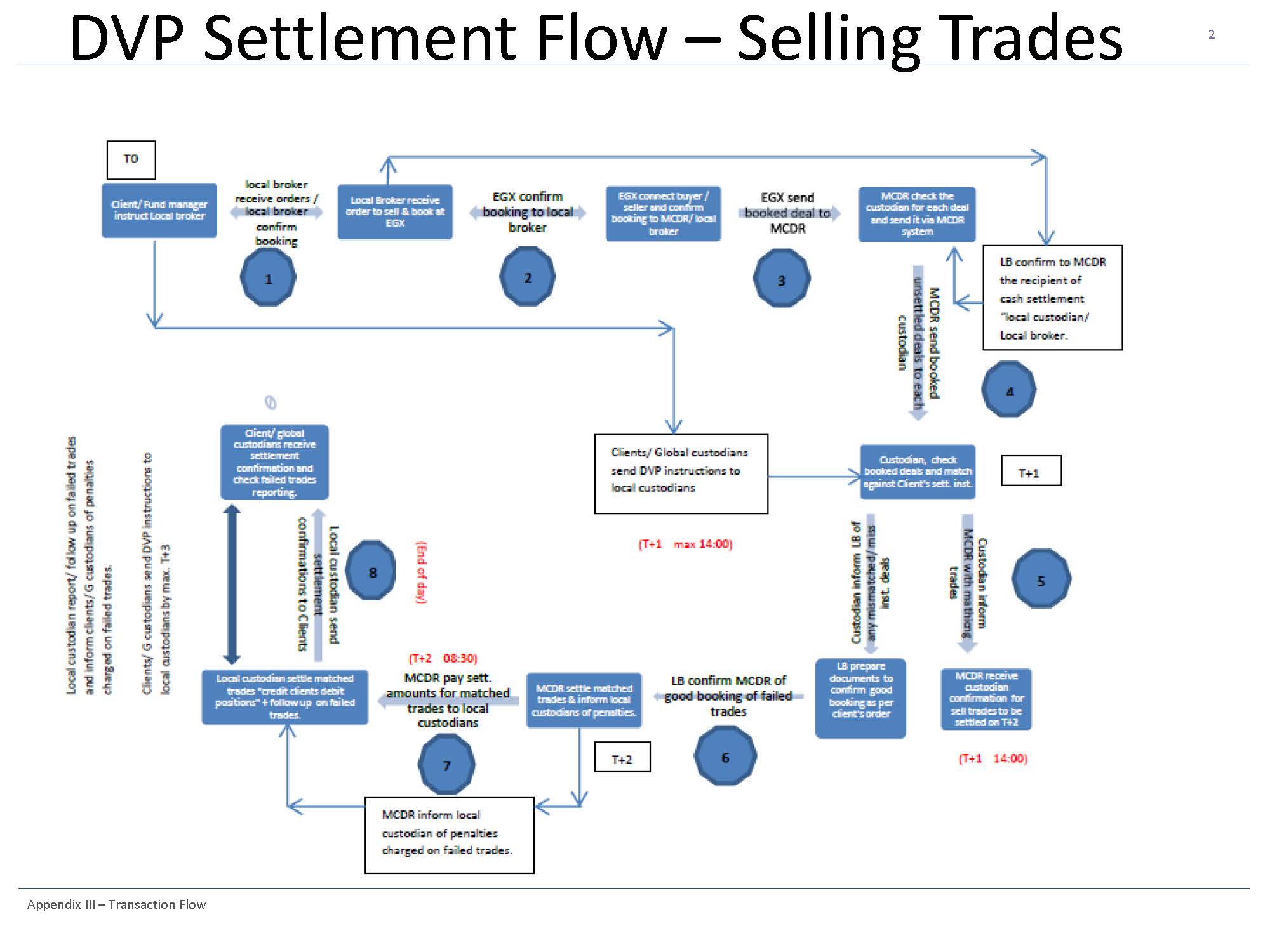

T-Bill instructions should be received by latest settlement date at 11:00 Cairo Time to avoid failure of the trade. The delivery-versus-payment (DVP) model was implemented in the market on March 1, 2016. Any trades executed from that date in the market will have a settlement cycle of T+2 for both purchase and sale transactions. This new model only impacts equities and corporate bonds. |

||||||||

|---|---|---|---|---|---|---|---|---|---|

| Delivery versus Payment (DvP) Settlement Currencies | EGP, USD & EUR |

||||||||

| Over-the-Counter (OTC) | There is no independent OTC market for equities. OTC trading must be executed through licensed brokers or through the EGX trading terminals. |

||||||||

| Settlement Procedures |

Purchase transactions: T+0:

T+1:

T+2:

Sale transactions: T+0:

T+1:

T+2:

Claims/Penalties process: The Settlement Guarantee Fund (SGF) penalty will be calculated at 0.5% of the trade amount for each day settlement is delayed, whether for purchase or sale transactions. It is worth highlighting that since Egypt is a beneficial owner's market, all penalties apply to the end client in case of delays, even if it is the international broker dealer’s mistake. Purchase Transactions:

Sale Transactions:

ADR/GDR cancellation details are as follows: - Client is kindly requested to coordinate with BNY as being the global depositary bank for any other requirements / documentations as subcustodian is concerned only with the local requirements.

ADR/GDR issuance details are as follows: For any company where the percentage of issued GDRs exceeds the percentage of freely traded shares, the company will only be allowed to cancel GDRs until the percentage matches the ratio of freely traded shares. This new rule comes into effect as of Wednesday, 10 August 2016. It does not replace the previous requirement where GDRs can only reach one third of the issuer company’s capital. - Client is kindly requested to coordinate with BNY as being the global depositary bank for any other requirements / documentations as subcustodian is concerned only with the local requirements. Market specific charges per conversion: Total Stock Exchange Fees are being rounded up to the nearest USD figure. |

||||||||

| Short Selling | MCDR activated short selling in the market from December 1, 2019. The relevant arrangements are as follows:

|

||||||||

| Turn-around Trades | Turn-around trades are not possible in the Egyptian market. However agency clearing is permissible. |

||||||||

| Clearing Agents | Central Bank of Egypt - regulates the banking industry, cash clearing and settlement. |

||||||||

| Depositories | Misr for Central Clearing, Depository & Registry (MCDR) - is the national depository as well as the securities clearing agent for listed securities (physical and book-entry). MCDR was incorporated under Capital Market Law No. 95 and its Executive Regulations became operational in October 1996 as Egypt’s official central clearing house and central depository. MCDR is regulated by FRA and has the following ownership structure: 45% brokerage firms; 5% stock exchange (EGX); 50% local custodians. |

||||||||

| Bank for International Settlements (BIS) Settlement Model | BIS is an international organisation which fosters cooperation among central banks and other agencies in pursuit of monetary and financial stability. The Committee on Payments and Market Infrastructures (CPMI) uses three common structural approaches, or models, to categorise the links between delivery and payment in a securities settlement system. Not applicable. |

||||||||

| Registration Process | Book-Entry: Depository-eligible securities are registered upon settlement. |

||||||||

| Registrar | Misr for clearing and Central Depository. |

||||||||

| Registration Period | Registration of physical securities takes place within one - four weeks and dematerialised securities are registered by default. Broker Authorisation Form Egyptian Market regulations require that local brokers request custodian banks to block securities before executing a sale trade based on an order placed with that broker by the client. Through this document, the Client authorises Citi Citibank N.A. Egypt to block securities on the Client's account at Misr for Central Clearing Depository & Registry (MCDR) on behalf of the authorised local broker. A list of all of the brokers with membership of the Egyptian Stock Exchange is available; please see the following link to the Misr for Central Clearing, Depositary Registry, http://www.mcsd.com.eg/mcdr/English/company.aspx?kindid=1 The Authorisation document may be completed with the names of the specific brokers, or a blanket authority may be provided in respect of all Egyptian Stock Exchange member brokers. Please complete this document on company letterhead. The Client may also choose to include all sub-account holders (investors) in the letter to provide blanket coverage in respect of investors under its Main Account to avoid the requirement for each of the sub account holders to also sign the Letter individually. To effect this, when signing the Letter, Client should ensure that along with the Company name in the bottom of the document to add "and all underlying sub accounts" or words to that effect. |

Risk

| Disclosure Requirements | Share holdings may be required to be disclosed by the beneficial owner, particularly when holdings reach or exceed prescribed disclosure limits. Investors must ensure that they comply in full by reporting such holdings to the appropriate organisations for this market, within the timeframe required. If you have any questions regarding this issue we encourage you to consult your legal counsel. Article 8 of Capital Market Law 95 for 1992 stipulates the following: -If the issuer company was publicly offered, the investor (a board member or an insider) has to inform the exchange, FRA, and the company if he intends to increase or buy a stake of 5 per cent or its multiples in a company (two weeks before the transaction). In the case of a normal investor and not a board member or an insider, the threshold is 10 per cent. The company, in return, notifies all the shareholders who have more than 1 per cent. -For listed companies, the threshold is stipulated by Chapter 3 in Article 332 and 333 of the executive regulations of Capital Market Law 95 for 1992, and it states the following: -Any person acquiring 5 per cent of the share capital or voting rights or its multiples of a listed company, or offered its shares to the public though not listed and not exceeding one third of such a company, has to disclose such acquisition to the Egyptian Stock Exchange and the FRA within two working days as of completion of the transaction. The notice has to identify the name of the acquirer, his holdings post-transaction, the name of the brokerage company and the name of the related parties - In case the acquisition reaches 25 per cent and does not exceed one third of the capital or the voting rights of the company, the acquirer has to disclose his future investment plan in respect of the management of the company, if any - The same rules apply if the acquirer is a board member and acquires 3 per cent or its multiples of the shares of such companies - A mandatory tender offer has to take place if the client's acquisition in a company reaches 33 per cent or more - Violation by the underlying investor will result in the cancellation of the transaction in question. Failure for a shareholder to disclose the necessary information would lead to fines not less than EGP2,000 and not more than EGP10,000 as documented under Law 95 for 1992, Article 67. In addition, article 21 of the said law shall apply, which stipulates that the chairman of the stock exchange may cancel any transactions that are effected in violation of the provisions of the law and its executive regulation. |

|---|---|

| Buy-Ins | Buy-In is enforced by the Settlement Guarantee Fund (SGF) which operates through the Depository (MCDR). For purchase transactions -On T+1, Local custodian has to accept the obligation for all matched trades on the MCDR screen by maximum 2 p.m. Cairo Time, where instructions are in place, valid, and with the appropriate funding by 10:30 a.m. Cairo Time. -On T+1 by 10:30 a.m. Cairo time, for instructions that fall under the following scenarios, the local custodian will not accept the obligation, which means the obligation for such transactions will automatically go to the local broker, and they have the option to fund the trade instead:

-Where the local custodian has not accepted the obligation, the shares will be pending on the MCDR system, available for acceptance by the local custodian once the instructions are in place. Where instructions/funding have been received after the settlement cycle, the local custodian will settle the transaction on their records, and credit the full amount to the local broker account (who has funded the trade initially). (Late confirmation penalties may be imposed by the local broker to the client.) In case where the local broker refuses to fund the transaction on behalf of the client on T+2 and presents the relevant supporting documentation to the Settlement Guarantee Fund (SGF) to prove the trade is valid, SGF will step in to lend the relevant trade amount to the seller and will start calculating a daily penalty on the buyer till settlement. The claim must be paid within 5 business days from the date it is charged.

For sale transactions -On T+1, Local custodian to accept the obligation for all matched trades on the MCDR screen by maximum 5 p.m. Cairo Time, where instructions are in place and valid by 10:30 a.m. Cairo Time. -On T+1 by 10:30 a.m. Cairo time, for instructions that fall under the following scenarios, the local custodian will not accept the obligation, which means the obligation for such transactions will automatically go to the local broker:

-where the local custodian has not accepted the obligation, and instructions have been received late after the settlement cycle, MCDR will credit the sale proceeds net of any penalties imposed by the SGF to the local custodian. Local custodian will calculate the total local broker commissions based on the invoices on the settled transactions and credit them to the local broker accounts. In case where the local broker has not provided the supporting documentation to prove trades executed are valid, all penalties will be imposed on the local broker. A buy-in will take place by the SGF on T+5, and the price difference will be charged to the local broker, along with the penalties.

Claims/Penalties process: -SGF penalty will be calculated at 0.5% of the trade amount for each day settlement is delayed. -Buy-in takes place on T+5 by the SGF, and any price differentials are charged to the defaulting party. -For late settlement of sale trades, sale proceeds are credited less the penalty amount. -For late settlement of purchase trades (where the local broker has refused to fund the trades), the penalty amount will be charged separately and must be paid within 5 business days. |

| Securities Lending | Refer to Short Selling section for details. |

| Compensation Fund | There is a Settlement Guarantee Fund (SGF) in place to settle the outstanding obligations of a defaulting broker. The liability of the fund will be limited to the amount of total cash contributions of brokers and the guarantee of the concerned broker. The SGF is under the responsibility of the Central Depository. |

| Anti-Money Laundering | Information not available |

Foreign Ownership

| Market Entrance Requirements | This is an FII market. Please contact your RBC Investor Services' Client Manager before making portfolio investments. |

|---|---|

| Investment Restrictions | There are no regulatory restrictions that limit foreign participation in the market or prohibit the repatriation of profits. However, there are few exceptions to this rule as some companies' charters do not permit foreign shareholders. |

| Repatriation Policy | Cancelled depository receipt sale proceeds are excluded from the CBE guaranteed repatriation mechanism. |

Cash

| FX Regulations | Effective December 3, 2016, the Central Bank of Egypt announced the free floating of the Egyptian pound. The interbank market has also been reactivated, 10:30 - 13:30 (local time) daily. |

|---|---|

| Payment Systems | Effective December 3, 2016, the Central Bank of Egypt announced the free floating of the Egyptian pound. The interbank market has also been reactivated. All transactions must be related to securities proceeds. There are currently two FX modules in Egypt, namely; the old mechanism/ interbank and the new Central Bank of Egypt (CBE) guaranteed mechanism, whereby the latter has been introduced on 17 March 2013 for foreign investors to repatriate their funds through the CBE with a premium. In other words, the CBE added a new option for the foreign investors to repatriate directly with the CBE in case they wish not to stand in the old mechanism queues, but at a higher price, provided that clients have originally obtained their EGP through the same mechanism. As for the old mechanism, an auction mechanism was established by CBE in 2012 through which banks can bid for certain percentages of the total auction amount and the allocation took place on pro-rata basis. As of 3 November 2016, CBE suspended the auction mechanism on the back of the current free-float regime being applied in the Market. Effective December 3, 2017, CBE announced changes to the repatriation mechanism (Foreign Investors Fund – FIF). Following the changes made to the spreads, clients have the option to come out of the CBE repatriation mechanism that was set up to guarantee the repatriation of funds. As a result, clients have the following two options:

CBE terminated the CBE repatriation mechanism. This applies to listed securities on the EGX, treasury bills, treasury bonds and corporate bonds. Effective December 5, 2018, any new FX inflows will be routed through the interbank market. Kindly note the pricing models as below : CBE FX Mechanism: Client Buying EGP selling FCY (USD) - the price announced on the CBEW1 page on Reuters at 2.00 pm Cairo time (CBEW1 Bid Rate) on the trade date ‘less’ 100 pips spread for the sub custodian (less applicable swap points), and 1% to CBE as a premium effective November 2017. Client Selling EGP buying FCY (USD) - the price announced on the CBEW1 page on Reuters at 2.00 pm Cairo time (CBEW1 Offer Rate) on the trade date . There will be a 0.5 per cent spread added to the CBEW1 offer rate (spread goes to CBE), and there will be no additional spread added by the local subcustodian bank. Investors will receive their FCY for spot value (I.E ASD+3). Pricing methodology and applied spreads are all mandatory and dictated by the Central Bank. The interbank market is quite volatile, the average daily volumes are around USD 80-100MM, but no official figures are announced. Interbank market does not guarantee repatriation in case of no liquidity. There is no fixed spread for interbank as market is dynamic and it depends on several factors i.e. demand and supply, market etc. |

| Overdraft Permitted | Up to four business days operational/technical overdraft can be arranged for foreign investors. |

Entitlements

| Dividend Process |

|

||||||

|---|---|---|---|---|---|---|---|

| Dividend Payment Frequency | Annual / semi-annual |

||||||

| Interest Payment Frequency | Interest on government bonds can be paid semi-annually in EGP through the MCDR for dematerialised bonds. |

||||||

| Interest Accrual Rate | Actual |

||||||

| Corporate Actions |

|

||||||

| Additional Information | The most common corporate actions in Egypt are:

Corporate actions are typically effected annually in either June and July or December and January after fiscal year-end of issuers on December 31 or June 30. |

||||||

| Protection of Rights | All rights are entitled according to trade date position, where reconciliation is done with the CSD prior to affecting any payment. |

Proxy Voting

| Foreign Investor Restrictions | Unrestricted voting rights |

|---|---|

| Shares Blocked | Yes, three business days before the annual general meeting, then unblocked on meeting day after the trading day is over. |

| Meeting Notices/Agendas | Yes, three business days before the annual general meeting, then unblocked on meeting day after the trading day is over. |

| Meeting Outcome | Regularly sent after the meeting is held. |

| Company Reports | Not available |

| Power of Attorney | Required |

| Other | Not applicable |

Taxation

| Dividend Tax Rate | Cash dividends are taxable with effective July 2, 2014, dividend tax as follows:

MCDR is coordinating, along with the Egyptian Tax Authority, the implementation of the double taxation treaties on Capital gains and cash dividends taxes. In that respect, they are preparing a full database for foreign clients investing in the Egyptian capital market and their eligibility for the reduced rates. Accordingly, they requested the sub-custodians to collect a notarized and consularized Certificate of Tax Residency (COTR) in addition to the Certificate of Beneficial Ownership (CBO) from all clients to be then provided to the MCDR. It is worth noting that clients who do not submit the said documents will not be eligible for the reduced tax rates. We suggest that clients seek further advice from professional tax consultants/advisers in that respect as subcustodian does not assume any responsibility with regard to tax-related issues since it is not part of our provided services.

Clients should complete the CBO form in accordance with the below:

ETA

authorised signer and stamped with the company/fund stamp

|

|---|---|

| Interest Tax Rate | Withholding tax applies on treasury bills and treasury bonds sale trades and redemption/coupon payments at a default rate of 20 per cent. Double Tax Treaty rates may apply if the client completes the Withholding Tax form and any documents that may be required at the time. The WHT on T-bills and bonds is calculated on maturity date or actual selling date. The WHT is calculated based on the difference of face value to purchase price/number of days to maturity representation the daily accrual realised by the investor’s holding period. |

| Capital Gains Tax Rate | Capital gains are taxable with effective 2 July 2014, it was calculated by MCDR and deducted from source, while clients are notified with the applied CGT through the local broker invoice, please note the related information as published in the MCDR https://www.mcsd.com.eg/mcdr/english/ The Egyptian government has decided to put the 10% tax on capital gains on hold for two years effective 17 May 2015, while MCDR refunded to clients capital gains taxes deducted from the period of 17 May 2015 till 24 August 2015. Suspension on CGT was further extended until 17 May 2020, noting that the 10% tax on stock dividends remains in effect. In March 2020, the government permanently exempted capital gain tax (CGT) on equities for non-residents. MoF issued directive number 610 for the year 2020 which introduces the applicability of Capital Gain Tax (CGT) on capital gains derived on unlisted equity stocks by non-resident investors effective on 14 December 2020:

|

| Tax Treaties | All information regarding the double taxation agreements is on the official web-site http://www.incometax.gov.eg/treaties.asp |

| Stamp Duty | Transactions conducted on EGX for both buyers and sellers will be subject to stamp duty. Both the buyers and sellers will pay the full rate. Stamp duty applied in stages as follows:

Stamp duty will be applied on all listed and non-listed Egyptian or foreign securities. Equities and corporate bonds will be impacted by Stamp Duty. Treasury Bonds, which are traded in EGX and settled at MCDR will not be impacted by Stamp Duty. Deductions are to be applied by MCDR that will accordingly transfer the stamp duty tax to the Egyptian Tax Authority. |

| Other Taxes | A 0.3% levy will be applied on investors acquiring 33% or more of shares or voting rights in a resident company for each the buyer and seller, as well as a 0.3% levy for investors acquiring 33% or more of the assets and liabilities of a resident company by another company for each the buyer and the seller. |

Holiday Calendar

Local Websites

|