Appointed subcustodians

Some markets are restricted for UCITS funds investment – please refer to your depositary team

INDIA

Updated as at October 27, 2023

Market Account Opening Requirements

FII Market Entry Requirements for India RBC IS operates a segregated account structure in this market. Please refer to 'Market Account Opening Requirements' for information on the market requirements. Clients are requested to refer to the requirements for information purposes only. For further information or support around accessing this market, please contact your RBC IS representative. |

Market Statistics

| Currency | Indian Rupee (INR) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Time Zone | GMT + 5 | |||||||||

| Bombay Stock Exchange Ltd (BSE) |

|

Market Infrastructure

| Exchange(s) | Currently 4 Stock Exchanges are recognised by the Securities Exchange Board of India (SEBI) located all over India, however, market activity is concentrated at The BSE Ltd (BSE) and the National Stock Exchange of India Ltd (NSE), which constitute 99% of the market share in terms of turnover (BSE has a market share of 22% and NSE has a market share of 77%). |

||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Trading System | BSE and NSE have automated online screen based trading systems, which allow orders to be placed at a “pre-determined” or “best” price. The automated screen based trading system for BSE is known as the BOLT (BSE on Line Trading) system and for NSE it is known as the NEAT (National Exchange for Automated Trading) system.

Price priority - of two orders entered into the system, the order with the best price gets the higher priority for trade matching.

[Please note that debt securities are mainly negotiated bilaterally and subsequently reported to the stock exchanges.] |

||||||||||||||||||||||||

| Trading Hours | Equities: |

||||||||||||||||||||||||

| Security Identifiers | ISIN (International Securities Identification Number): Used for all equities and dematerialised debt. |

||||||||||||||||||||||||

| Regulatory Bodies | Reserve Bank of India (RBI) - RBI was established under the Reserve Bank of India Act, 1934 and is the central banking authority of India. It regulates general banking, foreign exchange and money market operations. For Foreign Portfolio Investors (FPIs), the RBI has provided a general approval to open INR accounts (post receipt of SEBI approval), monitors overall foreign ownership limits and stipulates conditions for repatriation of funds. |

||||||||||||||||||||||||

| Instruments |

|

||||||||||||||||||||||||

| Form of Securities | Securities: can be held in dematerialised form only with the National Securities Depository Ltd (NSDL) or the Central Depository Services (Indian) Ltd (CDSL). Nearly all equities have been converted into dematerialised form The FPI regulations mandates FPIs to hold or transact securities only in dematerialised form. All unlisted public companies are required to issue securities in dematerialised form. It is compulsory for holders of securities of unlisted public companies to have such securities dematerialised before transfer and before subscribing shares under private placement or bonus shares or rights offer. Furthermore, SEBI amended the listing regulations to mandate the transfer of securities of listed companies in dematerialised form with effect from April 1, 2019. |

||||||||||||||||||||||||

| Board Lots |

|

||||||||||||||||||||||||

| Price Variations | The Minimum price variation unit is INR 0.01

If the normal market is closed due to Index based market-wide circuit filter breach anytime during the order matching period for a new listing of a security (IPO), relisting of a security, SME securities and illiquid securities period call auction, the matching process shall be completed.

|

||||||||||||||||||||||||

Settlement & Registration

| Settlement Cycles |

All the equity securities (including below securities listed on stock exchange) which were under T+2 settlement have been transitioned to T+1 rolling settlement effective from January 27, 2023. A FPI can participate in a Primary Auction of government securities. Similarly the Central/State Government in India or the Reserve Bank of India may purchase securities from FPIs through an Open Market Operation (OMO). Primary Market Settlement Cycle is T+1 for both Open Market Operation (OMO) and Primary Auction. The retail debt market lacks depth. The bulk of the market volumes are transacted on the Negotiated Trade Reporting (NT) segment of NSE. Transactions are reported by brokers on BSE and NSE NT are either settled on NSDL/CDSL for corporate bonds and the Negotiated Dealing System (NDS) of the RBI for Government bonds, through the Clearing Corporation of India Ltd (CCIL). .FPIs have been permitted to invest in unlisted corporate debentures/bonds subject to end use restriction on investment in real estate business, capital market and purchase of land. FPIs are also allowed to invest in securitised debt instruments. For secondary market government bonds trading, broker is not mandatory for FPIs. Further, SEBI has also provided flexibility to Category I & II FPIs allowing them to trade in corporate bonds directly and not through broker. The debt segment shall offer separate trading, clearing, settlement, reporting facilities and membership to deal in:

An FPI may purchase the following debt instruments on repatriation basis subject to the terms and conditions specified by the Securities and Exchange Board of India and the Reserve Bank: (a) dated Government securities/ treasury bills; (b) non-convertible debentures/ bonds issued by an Indian company; (c) commercial papers issued by an Indian company; (d) units of domestic mutual funds or Exchange-Traded Funds (ETFs) which invest less than or equal to 50 percent in equity; (e) Security Receipts (SRs) issued by Asset Reconstruction Companies; (f) debt instruments issued by banks, eligible for inclusion in regulatory capital; (g) Credit enhanced bonds; (h) Listed non-convertible/ redeemable preference shares or debentures issued in terms of Regulation 6 of these Regulations; (i) Securitised debt instruments, including (i) any certificate or instrument issued by a special purpose vehicle (SPV) set up for securitisation of asset/s with banks, Financial Institutions or NBFCs as originators; (j) Rupee denominated bonds/ units issued by Infrastructure Debt Funds; Provided this will include such instruments issued on or after November 22, 2011 and held by deemed FPIs. (k) Municipal Bonds : Provided that FPIs may offer such instruments as permitted by the Reserve Bank from time to time as collateral to the recognized Stock Exchanges in India for their transactions in exchange traded derivative contracts as specified in sub-Regulation 2 of Regulation 5.

(E) Risk Management: With the implementation of T+1 settlement for equity trades, there will not be any margins that will be collected from client. As per SEBI - Master Circular for Stock Exchange and Clearing Corporation – All transactions executed on the stock exchanges shall be settled through the Clearing Corporation/House of the stock exchange Please be informed that converting a trade into hand delivery may lead to the below:

Considering the above, we request you to send the trade instruction within the SCB deadline so that the trade can be confirmed on exchange. Please note that trade confirmation market deadline is 7.30am IST on T+1 and accordingly all trades need to be matched confirmed to clearing house. If not, then trades will settle via hand delivery mode before 10.20 am . Any un-confirmed trades will settle through hand delivery and may have associated penalties. Hand Delivery Settlement process for Purchase trade: In case of purchase trade i.e RVP trade which is converted to hand delivery mode, client will have to ensure that their valid matching instruction along with funds are place latest by 14.00 pm IST on T+1. In this case, the broker will receive the securities from the clearing corporation and same will be passed on by the broker to client’s account. Standard Chartered Bank will remit funds to the broker only after receipt of securities in client’s depository account with Standard Chartered Bank in order to secure the settlement process and eliminate the counterparty risk for the client. Hand Delivery Settlement process for Sale trade: In case of Sale trade i.e. DVP trade which is converted to hand delivery mode, client will have to ensure that their valid matching instruction are in place with Standard Chartered Bank before 8.30 am IST on T+1. This will enable Standard Chartered Bank to co-ordinate with the broker for settlement. Kindly note in case of Sale trade, the broker will have to ensure that they remit the funds to Standard Chartered Bank to secure the settlement process and eliminate the counterparty risk for the client. Post collecting funds from broker, Standard Chartered Bank will deliver the securities to the broker for settlement of trades. If securities are not delivered to the broker on value date (T+1 before 10.30 am IST -Market deadline), then it will result in buy-in of trade on the exchange platform. The broker will get charged for the buy-in cost and same may be passed on to the client for settlement with the broker. Note on penalties:

In case the exchange is unable to procure the required quantity of shares through the buy-in, the deal is closed out by paying the purchaser cash in lieu of the securities. In case the auction price is higher than the valuation price, the difference is debited to the account of clearing member delivering short. In cases where the valuation price exceeds the auction price, the excess is not returned to the party at fault for the short delivery. Such excesses are credited to the “Investor Protection Fund” maintained by the Exchange. Close-out: Where an auction does not deliver the quantity necessary to meet the shortage, the Exchanges close such shortages out, and deliver cash to the member receiving short (by a compensating debit to the member delivering short). The close-out price is the higher of:

AND

Penalty for Short Delivery: Besides incurring the cost involved in acquiring shares through the buy-in (or close-out), the defaulting delivering member is penalised. On the BSE & NSE, this penalty amounts to 0.05% per day of the contracted settlement value of the shortage.

For debt securities on institutional platform

Retail platform

Margins Upfront Margins on Non-Institutional Equity Trades

Based on the funding and early pay-in arrangement, local custodian could confirm the non-institutional trade and report to exchange that margin is collected from the client or early pay-in is done on T date itself. If local custodian cannot confirm the trade on T date, then the trade will devolve to broker and they need to provide and report margin to exchange for T day. The local custodian again will have option on T+1 to confirm the trade and report to exchange that margin is collected for T+1. In this case, broker still need to confirm margin for T+0 or will be penalised for any short collection / non-collection. Broker may pass on the funding cost or penalty to the client. The investor types considered as non-institution for this purpose are as follows:

|

||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Delivery versus Payment (DvP) Settlement Currencies | INR |

||||||||||||||||||||||||||||||||||||||||||||||||

| Over-the-Counter (OTC) | BSE and NSE are the primary exchanges for trading in equities. OTC trading in equities is therefore limited to unlisted securities. Further, regulations mandate that FPIs transact only on the floor of the Exchange through SEBI registered brokers. While debt instruments (government bonds and corporate bonds) are mainly negotiated bilaterally the corporate bond trades are required to be subsequently reported to the Stock Exchanges (reporting platform CBRICS (NSE) and ICDM (BSE)) and government bond trades on to Clearing Corporation of India Ltd (CCIL) through NDS-OM system. FPIs can invest in unlisted non-convertible debentures and securities debt instruments. However, investment in unlisted non-convertible debentures is subject to minimum residual maturity of above one year and end use-restriction on investment in real estate business, capital market and purchase of land. |

||||||||||||||||||||||||||||||||||||||||||||||||

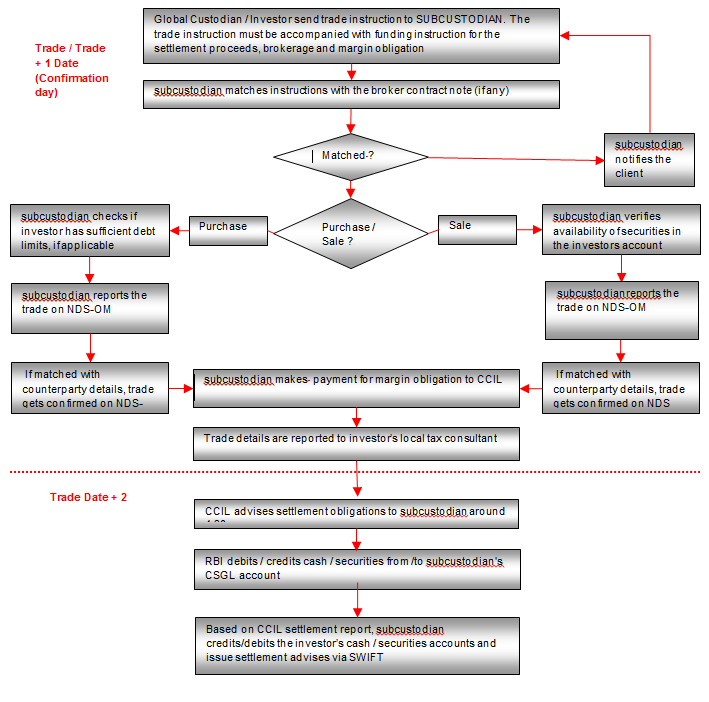

| Settlement Procedures | Equities: Equity trades follow a T+1 settlement cycle and clearing is affected by the clearing houses of BSE and NSE. The timelines for settlement on T+1 are: As mentioned, settlement is effected directly between the custodian and the designated clearing-house on T+1. Such trades need to be confirmed by custodian to the Clearing Houses by 07:30 IST on T+1 (i.e. confirm to the clearing house that the counterparty for settlement will be the custodian and not the broker). In case of non-confirmation, the obligation to settle the transaction automatically devolves on the broker through whom the trade has been executed. FPIs can execute OTC secondary market transactions in Government Securities with settlement cycle either as T+1 or T+2. However, all trades are required to be reported to NDS-OM on trade date itself. Settlement cycle for secondary market G-Sec trades undertaken by FPIs on NDS OM Web platform is T+1. The process flow for settlement of Equity Trades is detailed below:

MTM margins can be netted at the client level, for same day positions of the client i.e. the losses in some scrips can be set off/netted against profits of some other scrips. VaR and ELM cannot be netted because neither the VaR nor the ELM can take a negative value for any security to allow it to be netted with the VaR or ELM requirements of another security. In case there is a negative difference in VaR between TD and TD+1 (i.e. VaR of TD+1 < VaR of TD), VaR margin is not netted by the exchange and is only returned on TD+2.

In order to receive the cross margin benefit as per the first two cases, the basket of constituent stock futures / stock positions must be a complete replica of the index futures. Stock exchanges will specify the number of units of the constituent stocks / stock futures required in the basket to be considered as a complete replica of the index from time to time.

Please note that as per our subcustodian's discussions with NSE and BSE, investors are not required to enter into agreements with their custodian/ brokers to avail the cross margin benefit. Additionally, the file informing the cross margin benefit provided to investors will not be sent to the custodian/clearing member until 18:00 Indian Standard Time making it difficult for clients to avail of the cross margin benefit. When placing an order, the portfolio manager has to quote the following information to his broker:

Government securities: Settlement of all trades in government securities through CCIL is on a standardised T+1 basis. However, FPIs are allowed to settle their OTC secondary market G-Sec transactions either on T+1 or on T+2 basis. Trades are to be reported by both counterparties on NDS OM platform. NDS OM system is available on working days (Monday to Friday) until 17:00 IST. Both purchase and sale transactions are required to be reported and matched/confirmed on NDS OM reporting system before 17:00 IST on Trade day itself. All matched trades on NDS will be settled by CCIL after verification of risk exposure limits under guaranteed settlement. All trades (both purchase and sale) on NDS are to be backed by margins, which is a function of the margin factor announced by CCIL every fortnight. These margins are released one day after settlement of a trade. CCIL computes securities and funds obligation for each member and intimates RBI, who debits/credits respective securities accounts and funds accounts at the end of the day. RBI intimates CCIL on completion of transfers. The members in turn debit or credit securities and funds to clients' accounts. CCIL confirms the movement of securities on NDS at end of the day. Pre-matching: For Government Securities trades are matched by the buyer and seller on NDS. Trade confirmation: Government securities to be settled with CCIL are required to be confirmed on NDS.

Important Note: In addition to the current matching parameters, which form part of trade instructions, two additional parameters viz. the time the deal was struck and the counterparty name have been introduced as a matching criteria. Thus, for the purpose of order matching, the time the deal was struck between the buyer and seller and the name of the counterparty must mirror. The process flow is explained diagrammatically here:

Note: The Margin amount collected on the Confirmation day, will be refunded to the client’s cash account on Settlement Day +1. Effective December 1, 2016, FPIs have been permitted to trade Government securities in the secondary market through Negotiated Dealing System – Order Matching (NDS-OM) Web module. Trades executed on this module are settled on T+1 basis only. FPIs intending to access NDS-OM Web platform for direct dealing in secondary market G-sec transactions are required to obtain digital signature certificate for registration on NDS-OM Web. Trades executed on this platform would require pre-funding. Corporate debt: Transactions shall be reported on F-TRAC by eligible participants only in respect of those trades which are required to be reported on F-TRAC as per the directives/ circulars issues by the SEBI, the RBI or any other competent regulator in respect of the concerned market from time to time. Both the counterparties to every trade are required to report accurately and completely all relevant details of the trade as stipulated/required for F-TRAC, as set out in the attached document or as communicated by FIMMDA from time to time. Consequent to reporting of trade details by both the counterparties they will be matched internally by the F-TRAC and upon matching, market related information would be disseminated on the F-TRAC and FIMMDA website The above mentioned reporting process is applicable only for CP and CD trades. However, currently FPIs are not permitted to invest in CPs and CDs. However, FPIs can invest in CPs through Voluntary Retention Route (VRR) for debt market investments.

Settlement procedure:

Effective December 7, 2009, corporate bonds listed on the BSE will settle through the through the Indian Clearing Corporation Limited (ICCL). Three settlement cycles, trade date (T)+ 0, T+1 and T+2, will be available for reported transactions. Pay-in timelines are as follows:

The pay-out of funds/securities will be processed within one hour of the pay-in deadline. Additional settlement cycles for T+1 and T+2 deals may be provided in the future.

Custodian confirmation can be done up to 15:00 on trade date for T+0 settlement and up to 10:30 on the respective settlement days in the case of T+1 and T+2 settlement.

The process flow for trades executed through the ICCL is detailed below:

Corporate Bonds/ Commercial Papers through Indian Clearing Corporation Limited (ICCL)

Currently, FPIs are not permitted to invest in Commercial Papers (CPs) and Certificate of Deposits (CDs). However, FPIs investing in debt markets under Voluntary Retention Route (VRR) are allowed to invest in CPs. |

||||||||||||||||||||||||||||||||||||||||||||||||

| Short Selling | In India “Short selling” is defined as selling a stock which the seller does not own at the time of trading. |

||||||||||||||||||||||||||||||||||||||||||||||||

| Turn-around Trades | This is not permitted in the Indian capital market. |

||||||||||||||||||||||||||||||||||||||||||||||||

| Clearing Agents | Both the main stock exchanges in India i.e. the BSE Limited and the National Stock Exchange of India Limited (NSE) have their own clearing houses which take care of the settlement and clearing of trades executed on these stock exchanges. |

||||||||||||||||||||||||||||||||||||||||||||||||

| Depositories | National Securities Depository Ltd (NSDL) and Central Depository Services (India) Ltd (CDSL) - act as depositories for Equity, Corporate Debt and some Government Securities. They are incorporated under the Companies Act, 1956 as public limited companies limited by shares and are for profit institutions. NSDL and CDSL facilitate clearing of trades through depository participants, by enabling securities transfers across beneficial owners, inter-se and to/from clearing members, based on transfer instructions. |

||||||||||||||||||||||||||||||||||||||||||||||||

| Bank for International Settlements (BIS) Settlement Model | BIS is an international organisation which fosters cooperation among central banks and other agencies in pursuit of monetary and financial stability. The Committee on Payments and Market Infrastructures (CPMI) uses three common structural approaches, or models, to categorise the links between delivery and payment in a securities settlement system. |

||||||||||||||||||||||||||||||||||||||||||||||||

| Registration Process | Securities are registered in the name of the beneficial owner (in the name registered with SEBI in case of FPIs). Omnibus and nominee account structures are not recognised in India. |

||||||||||||||||||||||||||||||||||||||||||||||||

| Registrar | A registrar provides a service to listed companies. The core tasks of a registrar are: |

||||||||||||||||||||||||||||||||||||||||||||||||

| Registration Period | Depending on the securities involved, registration can vary from 30 to 60 days. Please note that stamp duty has to paid at the time of sending the shares for registration. |

Risk

| Disclosure Requirements | Shareholdings in this market may be required to be disclosed by the beneficial owner, particularly when such shareholdings reach or exceed prescribed disclosure limits. Investors must ensure that they comply in full by reporting such holdings to the appropriate organisations, within the specified timeframe. If you have any questions regarding this issue we encourage you to consult your legal counsel.

SEBI (Substantial Acquisition of Shares & Takeovers) Regulations, 2011: as per these regulations, an acquirer (with persons acting in concert*) is required to make an initial disclosure is required on acquisition of 5 per cent or more shares or voting rights. The disclosure has to be made upon receipt of intimation of allotment of shares, or the acquisition of shares or voting rights in the target company to the target company at its registered office and every stock exchange where the shares are listed within 2 working days. Standard Operating Procedure for seeking additional disclosures from certain objectively identified Foreign Portfolio Investors (FPIs), in accordance with SEBI circular no. SEBI/HO/AFD/AFD-PoD-2/CIR/P/2023/148 dated August 24, 2023

For commercial establishments and corporate group pension funds, the DDP shall verify the name of the pension fund from the websites of the regulators / government / state authorities (provided in Annexure B) and obtain an original or duly attested/ certified document filed with/ obtained from some regulator / government / state authority, which corroborates that the FPI is in the nature of a pension fund. For pension funds falling in points (ii) to (iv) above, the DDP shall either verify the name of the pension fund from the websites of the regulators / government / state authorities (provided in Annexure B) or rely upon an original or duly attested/ certified document filed with/ obtained from some regulator / government / state authority, which corroborates that the FPI is in the nature of a pension fund.. The certification/ attestation shall be carried out by people authorized to do the same as per the Master Circular for FPIs and DDPs.

A list of regulated pool structures from various jurisdictions along with the names of regulators and relevant web – links is provided in Annexure D.

Notes:

*Actual date may vary based on the holiday calendar published by the stock exchanges from time to time Notes:

Notes:

‘We understand that our FPI group is currently breaching the INR 25000 crore limits as prescribed in the SEBI circular no. SEBI/HO/AFD/AFD - PoD - 2/CIR/P/2023/148 dated 24 August 2023. In this regard, we declare that we do not intend to undertake any trade in equities in the Indian securities market. and agree for our account to be blocked for equity purchase so that we may be exempted from providing additional granular disclosures as per the said circular. We further undertake and understand, that in the event we choose to trade in Equities, we shall inform the same to our DDP/ Custodian beforehand so that the account can be unblocked for fresh equity purchases. Thereafter, we shall be obligated to comply with the requirements and timelines mentioned in the aforementioned SEBI circular, including granular disclosure requirement, as applicable on the FPI investor group of whom we are a part.’ As stated in the declaration, before taking any fresh equity position, the FPI shall inform the same to the DDP/ Custodian for unblocking its account post, which, the DDP shall unblock the account and forthwith, included such FPIs for the purpose of monitoring and additional disclosures. The requirements applicable on the FPI investor group shall become applicable on the FPI from the date the FPI expresses its desire to starts trading in the equity segment. For instance, in case the FPI investor group is in the mandatory disclosure period on the date, the FPI expresses its desire to starts trading in the equity segment; such FPI shall also be required to make the disclosures during the mandatory disclosure period applicable for the FPI investor group.

Government and Government related investors registered under Regulation 5 (a) (i) of the FPI Regulations are exempted from providing such acknowledgment

Suppose as on July 01, 2023, the FPI has liquidated some shares and holds 15 shares of Company A and 30 shares of Company B. As on this date, the FPI will be able to exercise voting rights corresponding to 15 shares of Company A but only 20 shares of Company B (maximum permissible voting rights in Company A).

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Buy-Ins | Exchanges have instituted buy-in (auction) procedures that will kick in where a delivering member does not meet obligations. The exchange conducts auctions to acquire shortages from the market i.e it purchases the required quantity (the short delivery) from the market and delivers them to the original buying member. The buy-in schedules for T+1 settlement is as under:

In case the exchange is unable to procure the required quantity of shares through the buy-in, the deal is closed out by paying the purchaser cash in lieu of the securities. In case the auction price is higher than the valuation price, the difference is debited to the account of clearing member delivering short. In cases where the valuation price exceeds the auction price, the excess is not returned to the party at fault for the short delivery. Such excesses are credited to the “Investor Protection Fund” maintained by the Exchange. Close-out: Where an auction does not deliver the quantity necessary to meet the shortage, the Exchanges close such shortages out, and deliver cash to the member receiving short (by a compensating debit to the member delivering short). The close-out price is the higher of:

AND

Penalty for Short Delivery: Besides incurring the cost involved in acquiring shares through the buy-in (or close-out), the defaulting delivering member is penalised. On the BSE & NSE, this penalty amounts to 0.05% per day of the contracted settlement value of the shortage. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Securities Lending | Securities lending and borrowing (SLB) in India follows an exchange centric model where SLB transactions take place on screen-based trading platforms similar to those in cash / equity segment. The trading platforms are maintained by stock exchanges with their clearing corporation / house acting as central counter-party to all SLB transactions. The trading is anonymous i.e. the lender or borrower's identity is not disclosed to the counterparty. Salient features of the SLB model are:

Eligible Securities

In case of record date or closure of register of a company in any of the eligible security, such security will not be available for lending and borrowing for a period starting 7 days prior to record / closure date to 7 days after the record / closure date. SLB will be permitted in dematerialized form only.

Early Recall / Repayment

In case of an early repayment by a borrower:

Clearing and Settlement

Trade date +1

Reverse leg

Reverse leg + 1

In case securities are not bought through the buy-in auction, the trade will be closed-out. The computation methodology and rate of close-out shall be intimated by the exchanges from time to time. Dividend: The dividend amount would be worked out and recovered from the borrower on the book closure/ record date and passed on to the lender. Annual General Meeting (AGM) / Extraordinary General Meeting (EGM): In the event of the corporate actions which is in nature of AGM/EGM, presently the AIs are mandatorily foreclosing the contracts. It has been represented by market participants that mandatory foreclosure during the life of the contract may not be necessary as, all lenders may not be interested in taking part in the AGM/EGM. It has therefore been decided that the AIs shall provide the following facilities to the market participants:

Foreclosure of Transactions Introduction of roll-over facility

c) Rollover shall not permit netting of counter positions, i.e. netting between the ‘borrowed’ and ‘lent’ Shortages and close out rate

Early recall - 100% of the lending fee |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Compensation Fund | NSE Clearing and ICCL maintains Core Settlement Guarantee Fund (Core SGF). |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Anti-Money Laundering | RBI has prescribed anti-money laundering measures for banks,financial institutions and intermediaries operating in India under aegis of Prevention of Money Laundering Act, 2002. |

Foreign Ownership

| Market Entrance Requirements | This is an FPI market. Please contact your RBC Investor Services' Client Manager before making portfolio investments. An FPI has to obtain a certificate of registration prior to buying, selling or otherwise dealing in securities. The certificate of registration is granted by a DDP on behalf of SEBI.

As per SEBI press release dated February 25, 2020, when a jurisdiction is placed under increased monitoring, it construes that the country has committed to resolve swiftly the identified strategic deficiencies within agreed timeframes and is subject to increased monitoring. FATF does not call for enhanced due diligence to be applied to these jurisdictions but encourages its members to take into account this information in their risk analysis. FPIs from these jurisdictions can continue undertaking their investments in India but may be subject to increased monitoring. Foreign portfolio investors have to register with a DDP before they can invest in the Indian securities market.

Re-categorization of existing FPIs: In accordance with the SEBI (FPI) Regulations, 2019, existing FPIs are re-categorized as under:

Any FPI wanting to be re-categorized from Category II FPI to Category I, cab request to DDP along with requisite information, documents and payment of applicable fees.

Registration Fees for every block of 3 years

Applications for renewal of the approval along with the additional information, if any and supporting documents must be made prior to the expiry of the existing approval, at least 15 days before the expiry of the registration. The applicant is a resident of a country whose securities market regulator is a signatory to IOSCOs MMOU (Appendix A Signatories) or a signatory to bilateral MoU with SEBI;

Financial Action Task Force (FATF) has included Cayman Islands under the ‘Jurisdictions with strategic deficiencies’. Enhanced KYC monitoring is encouraged for FPI applications from this jurisdiction. Foreign investors have to open separate types of accounts in India for different asset holdings: FDI, FVCI and VRR require special processing that needs to be agreed first with RBC Investor Services before investment and account opening. FVCI also requires registration with SEBI under the SEBI (FVCI) regulations. FPIs are also required to obtain and submit a Permanent Account Number (PAN) card. Accounts on the depository (National Securities Depository Limited and / or Central Depository Services (India) Limited) will be opened only after receipt of the PAN card and verification of the same with the Income Tax web site. Registration on CORE

KRA KYC Form |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Investment Restrictions | The purchase of equity shares of each company by a single foreign portfolio investor or an investor group shall be below ten percent of the total paid up capital of the company on fully diluted basis. In the event an FPI and its investor group reach 10% or more of the total paid up equity capital of a company on a fully diluted basis, they must follow extant FEMA rules in this regard. The FPIs investing in breach of the prescribed limit shall have the option of divesting their holdings within 5 trading days from the date of settlement of the trades causing the breach. If such FPI and its investor group opt not to divest and wants to treat their entire investment into a company as FDI, such FPI including its investor group shall not make further portfolio investment. Such FPI/ its investor group shall inform respective custodians of the choice who in turn will report this to the SEBI, depositories and the issuer. Such investments shall be treated as FDI subject to norms as prescribed by RBI from time to time and will be marked as FDI in custodian records. However, FPI and its investor group will be able to sell these securities only through the route as they were acquired and appropriate reporting (i.e. LEC reporting) will be made by the respective custodian. As per the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 notified on 17 October 2019, a person resident outside India may hold foreign investment either as FDI or as FPI in any particular Indian company. Certain foreign government agencies and their related entities may be exempt from clubbing of investment limits and other investment conditions if the Government of India has entered into a relevant agreement or treaty with the sovereign government, or issued a relevant order.

Monitoring foreign investment limits in listed companies: The onus of compliance with the various foreign investment limits rests on the Indian company receiving such foreign investments. In order to facilitate listed Indian companies to ensure compliance with the various foreign investment limits, SEBI in consultation with RBI, has notified a new framework for monitoring the foreign investment limits. SEBI vide circular no. IMD/FPIC/CIR/P/2018/61 dated 05 April 2018 notified this framework which is operational since 01 June 2018. The salient features of this framework are as under:

Trade Reporting:

Activation of a Red Flag Alert:

Breach of foreign investment limits and Disinvestment methodology:

Example: A FPI XYZ purchases 1000 shares of ABC Ltd on 01 April. At the end of the day on 01 April, if NSDL detects breach in the permissible limit for ABC Ltd, FPI XYZ will be identified for proportionate disinvestment in the manner as explained in the above table. On 03 April, trade of 1000 shares of ABC Ltd will settle in the account of XYZ. Accordingly, disinvestment period of 5 trading days will begin from 04 April onwards. (Assumption: There are no trading/public holidays falling on any days from 01 April to 04 April)

Breach/Ban List:

The earlier monitoring mechanism by RBI has been discontinued.

Debt Securities The primary responsibility of complying with all the debt investment limits and conditions (stipulated by RBI and SEBI from time to time) lies with the FPI. Depositories shall monitor the investments at the investor group level while custodians shall monitor the investments of their own clients. The FPI debt investment limits applicable are as under:

Corporate Debt

Once the aggregated FPI investment reaches 95%, the following procedures will be adopted for allocating the unutilized limits for FPIs:

Government debt

Voluntary Retention Route (VRR) In addition to the normal debt investment limits mentioned above, RBI has introduced the VRR as a separate channel to enable FPIs to invest in debt markets in India. Investment under this route was initially capped at INR 400 billion for Government securities and INR 350 billion for Corporate bonds. Later, in second tranche, RBI notified VRR-combined (capped at INR 547 billion) which is fungible and can be used for investment in Gsecs as well as corporate bonds. The minimum retention period is three years or as decided by RBI for each allotment. Currently, VRR scheme first opened for allotment on a ‘first come first served’ basis until 31 December 2019 or till limits are exhausted whichever is earlier. Successful allottees must invest 75% of allotted amount within six months and are required to maintain minimum 75% of allotted amount throughout the retention period. Investments made by FPIs under VRR,are exempt from any minimum residual maturity requirement, concentration limit or single/group investor-wise limits applicable to corporate bonds. RBI has also notified that the hedging of exchange rate risk by FPIs under VRR through forwards, options, cost reduction structures and swaps with Rupee as one of the currencies. FPIs are required to open separate securities and cash account for VRR investments. RBI increased the limit under this route to INR 1,500 billion. An additional limit of INR 906 billion (net of existing allotments and adjustments) is available on tap from January 24, 2020 to FPIs. The Reserve Bank of India (RBI) has introduced a separate route through Fully Accessible Route (FAR) to enable non-residents to invest in specified Government of India dated securities, with effect from April 1, 2020. This scheme will operate along with the two existing routes, i.e. the Medium Term Framework (MTF) and the Voluntary Retention Route (VRR). The following are the key features of FAR:

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Repatriation Policy | FPIs are free to repatriate the capital, capital gains, dividends, interest and other income after payment of applicable taxes. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Cash

| FX Regulations | All local custodian in the India market have decided to charge investors a flat fee of INR 100 for each FX transaction executed by them. Each FX transaction includes all FX deals (purchase and sale separately) executed for each account at a single point of time with the same FX rate. RBI has made the Legal Entity Identifier (LEI) mandatory for all non-individuals participating in government securities markets, money markets and non-derivative foreign exchange markets. Investors who do not have their valid LEI may not be able to undertake transactions in government securities, money markets and non-derivative FX (settling up to SPOT date). LEI is not required for trades value less than USD 1 million (approximately INR 70 million). |

|---|---|

| Payment Systems | Cash clearing is both manual and electronic, in the case of manual clearing the payments are effected by delivery of cheques.Clearing of cheques may take 2-3 days depending on the location at which the cheque is drawn. Effective April 1, 2021, RBI will introduce the LEI requirement for large value transactions (INR 500 million and above) in the Centralised Payment Systems. |

| Overdraft Permitted | Local regulations in India do not permit funding of FPI investment through overdraft or other sources. Regulations also prescribe aggregation relationships, therefore, zero balance accounts, pooling etc. is not available across sub-accounts of a FPI, or across FPIs for a global custodian/DDP. |

Entitlements

| Dividend Process | Dividends are ex-date driven. Payment is made electronically through banking system. |

||||||

|---|---|---|---|---|---|---|---|

| Dividend Payment Frequency | Varies with issue, although normally annually. |

||||||

| Interest Payment Frequency | Varies with issue, although usually semi-annually. |

||||||

| Interest Accrual Rate | Government Debt – 30/360 day basis |

||||||

| Corporate Actions |

|

||||||

| Additional Information | To declare a corporate event, such as a dividend or bonus issues, the company must notify the relevant stock exchanges at least before the books close/record date. However, if company has been mandated to be compulsorily traded in dematerialised form, this period is reduced to 21 days. Margins |

||||||

| Protection of Rights | Ex-dates is used to determine whether corporate benefits are due to the investor or not, depending on the execution date of the trades done during this period. An ex-date is the date before which, if that particular stock is bought on the exchange, the buyer is entitled to receive the entitlements (dividend/rights/bonus). |

Proxy Voting

| Foreign Investor Restrictions | Foreign investors are entitled to exercise voting rights, with restrictions (e.g. a maximum cap is specified for voting rights for an Investor in a Private Sector bank). |

|---|---|

| Shares Blocked | No. |

| Meeting Notices/Agendas | Provided in English. General meetings are announced three weeks in advance. |

| Meeting Outcome | On request, subject to availability. |

| Company Reports | On request, subject to availability. |

| Power of Attorney | Required. |

| Other | Voting is executed by a show of hands unless a poll is demanded. A proxy may demand a poll if they hold 10% of the voting rights or INR 50,000 paid up capital. Proxies can only vote if there is a poll. |

Taxation

| Dividend Tax Rate | Effective April 1, 2020, the dividend distribution tax (DDT) paid by the companies is removed and dividend income will now be subject to Withholding Tax (WHT) at the rate of 20% plus applicable surcharge and cess. The maximum surcharge of 15% would be applicable on dividend income. The total WHT applied (20% + surcharges & cess) will be calculated by the issuing company based on the dividend threshold tiering. For all dividend income received post April 1, 2020, the investor’s local tax consultant has to provide the local subcustodian with a tax clearance certificate prior to repatriation. In case the tax to be paid is more than what the company has deducted at source, RBCIS has a standing instruction in place with our subcustodian who will withhold the differential amount as advised by the investor’s local tax consultant and pay it to the tax authorities and then repatriate the balance. There is no need for a separate instruction making the tax payment. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Interest Tax Rate | Withholding tax on interest is withheld at source by the issuing company. The rates could however be different in cases where the beneficial rates are applicable as per the Double Tax Avoidance Agreement (DTAA) with other countries. The following table provides the tax rates for interest for FPIs:

The above mentioned tax rates are inclusive of surcharge and cess. Reduced tax rate on interest for investment in Government Securities and Corporate bonds Interest paid to FPIs between 1 June 2013 and 30 June 2017* on Government securities and rupee denominated bond will be taxed at 5 per cent instead of 20 per cent. *As per the Union Budget for 2017-18 proposal, this benefit will be extended till 30 June 2020. The benefit of reduced withholding tax rate in respect of rupee denominated bond of an Indian company was applicable to bonds where the interest rate of the bond does not exceed the rate notified by the Government. As per the notification, for bonds issued before the 1 July 2010, the rate of interest shall not exceed 500 basis points (bps) over the Base Rate of State Bank of India (SBI) as on the 1 July 2010. Accordingly, for bonds issued before 1 July 2010, the cap on the interest will be 12.50 per cent (SBI base rate of 7.50 per cent as of 1 July 2010 + 5 per cent). For bonds issued on or after the 1 July 2010, the rate of interest shall not exceed 500 bps over the Base Rate of SBI applicable on the date of issue of the said bonds. Accordingly, for bonds issued on or after 1 July 2010, the cap on the interest will depend on the SBI base rate at the time of issue of such bonds. The SBI base rate is available on SBI’s website www.sbi.co.in. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

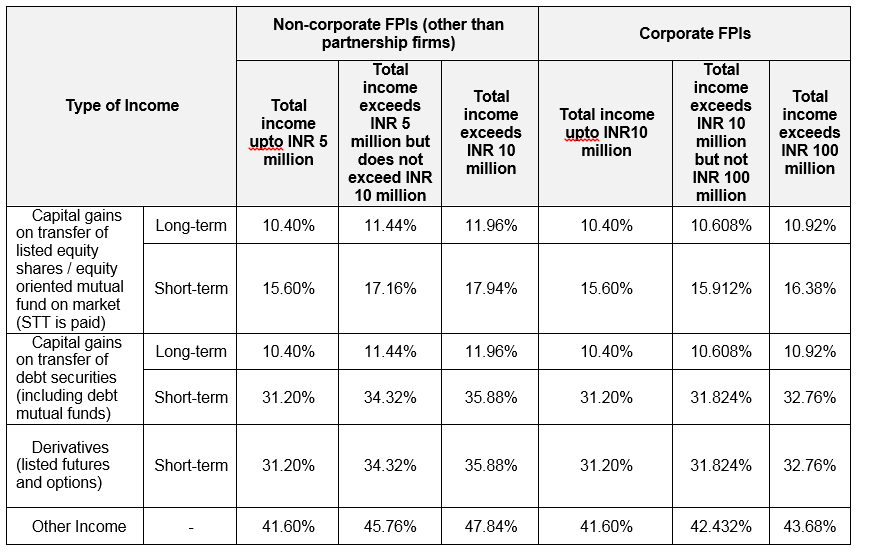

| Capital Gains Tax Rate | Indian tax laws mandate payment of capital gains tax (CGT) on the profits derived from sale of securities held by all categories of investors (including foreign investors). The standard CGT rates applicable to Foreign Portfolio Investors (FPIs) are as follows:

Non-corporates

Corporates

Long Term Capital Gains (LTCG)

General

Tax Filing on Sale of Underlying Shares Converted from ADR/GDR/FCCB

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Tax Treaties |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stamp Duty | The Finance Bill 2019 (Interim Union Budget for financial year 2019-20) introduced amendments in the Indian Stamp Act, 1899. Through these amendments, exemption from stamp duty levy applicable to transfer of securities in dematerialised form and transfer of units of mutual funds was withdrawn. Additionally, stamp duty rate (furnished below) were inserted in the Stamp Act along with by whom such stamp duty would be payable. The provision has also been made for centralized collection of stamp duty by stock exchanges or clearing corporations authorized by it or depositories. These amendments will come into force on Thursday, 09 January 2020. Implementation of the revised rules on the stamp duty payable on instruments transacted on stock exchanges and depositories will be effective from July 1, 2020.

The stamp duty rates will be payable by following:

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other Taxes | All taxes applicable to FPI transactions must be paid prior to repatriation of funds. Repatriation can be effected after the No Objection Certificate (NOC) is obtained from a tax consultant.

Advance Tax While the tax year runs from April 1 to March 31, taxes need to be estimated in advance and paid in instalments to the tax authorities. Taxes become payable by the 15th of each quarter, i.e. June 15, September 15, December 15 and March 15. Accordingly, advance taxes on trades executed from the last date on which tax was paid until the current quarter need to be considered when computing the amount of advance tax payable. If advance tax is not paid correctly, investors would need to pay interest.

Securities Transaction Tax (STT) STT was introduced as per Finance Bill 2004 on taxable security transactions executed on stock exchanges. The effective STT rates are as under:

Goods and Services Tax (GST) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Holiday Calendar

Local Websites

|