Appointed subcustodians

Some markets are restricted for UCITS funds investment – please refer to your depositary team

Norway

Updated as at December 19, 2023

Market Account Opening Requirements

RBC IS operates an omnibus account structure in this market. For further information or support around accessing this market, please contact your RBC IS representative. |

Market Statistics

| Currency | Norwegian Krone (NOK) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Time Zone | GMT + 1 | ||||||||

| The Oslo Børs |

|

Market Infrastructure

| Exchange(s) | Oslo Børs Equity Market The Oslo Stock Exchange was established in 1819 and is the principal market for trading of shares, bonds and other financial instruments in Norway. Norway has a relatively small securities market, with one stock exchange, the Oslo Børs. Euronext and Oslo Børs trading system is called Optiq and is used for equities and fixed income markets. Equity and equity-related instruments are normally placed on the Norwegian market via IPO (Initial Public Offering). For the secondary market there are currently three main listing alternatives in Norway:

Fixed Income Market |

||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Trading System | Euronext and Oslo Børs trading system is called Optiq and is used for equities and fixed income markets. Omgeo CTM is Omgeo’s strategic platform for the central matching of fixed income and equity transactions to further streamline trade flows, decrease operational risk, and increase efficiency. Omgeo CTM processes both cross border and non- U.S. domestic trades, and offers exception only processing, real-time settlement instruction enrichment, and automated settlement notification to custodians and interested third parties.

|

||||||||||||||||||||

| Trading Hours |

|

||||||||||||||||||||

| Security Identifiers | ISIN (International Securities Identification Numbering): Yes |

||||||||||||||||||||

| Regulatory Bodies | The Royal Norwegian Ministry of Finance |

||||||||||||||||||||

| Instruments |

|

||||||||||||||||||||

| Form of Securities |

|

||||||||||||||||||||

| Board Lots |

|

||||||||||||||||||||

| Price Variations | The tick size varies from NOK 0.01 to NOK 1.00 depending on size and liquidity of the shares |

Settlement & Registration

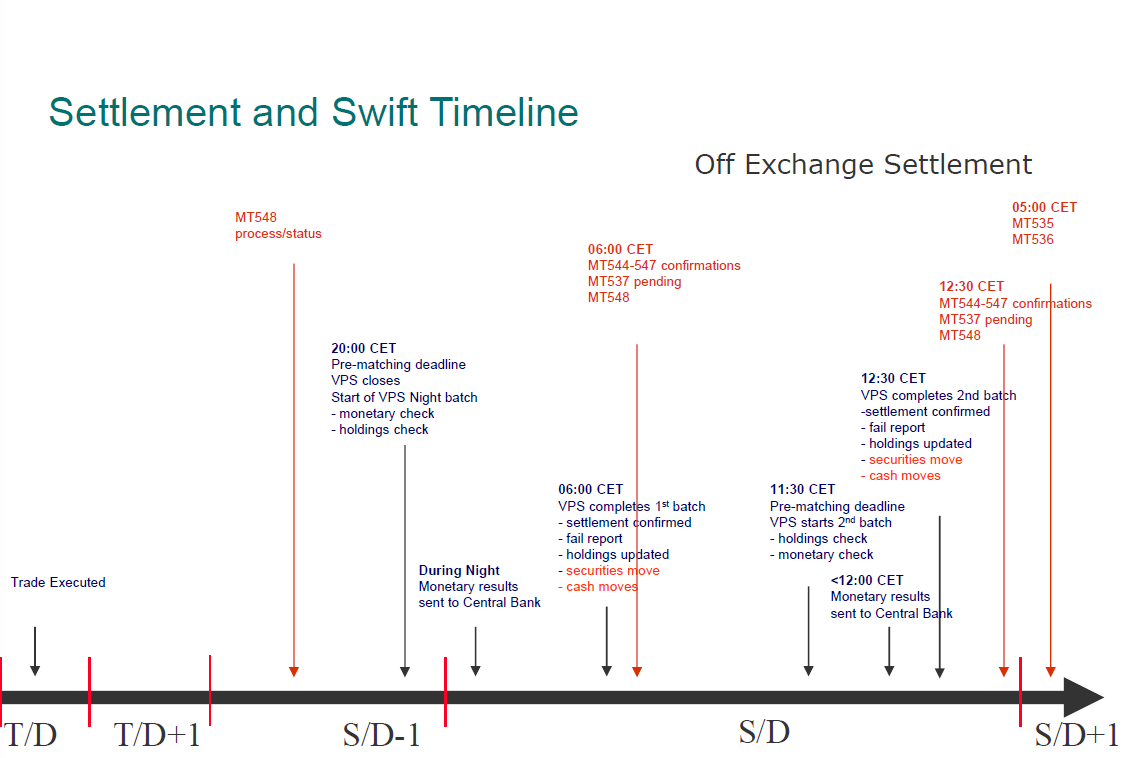

| Settlement Cycles |

* Note: Negotiable between parties - to a minimum of T+0 |

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Delivery versus Payment (DvP) Settlement Currencies | EUR & NOK |

||||||||||

| Over-the-Counter (OTC) | The Norwegian Securities Dealers Association developed a trading board to centralise the buying and selling of unlisted companies. |

||||||||||

| Settlement Procedures | Book-Entry: Clearing and settlement takes place three times during a twenty-four hour settlement period: First Settlement Cycle: Second Settlement Cycle: Third Settlement Cycle: |

||||||||||

| Short Selling | The Norwegian Parliament has passed changes to the Norwegian Securities Trading Act on naked short selling. |

||||||||||

| Turn-around Trades | Same day turnaround can be achieved in the market. Please note that there is no internal settlement, as all trades must settle at the CSD. |

||||||||||

| Clearing Agents | Central counterparty clearing (CCP) LCH Limited (LCH), European Central Counterparty N.V. (EuroCCP) and SIX x-clear Ltd are the current CCP service providers in Norway. Equity instruments and derivatives traded on Euronext Oslo (Oslo Børs), are cleared through a CCP. Members must set up clearing arrangement in order to trade these products on the Oslo Børs marketplaces. |

||||||||||

| Depositories | Euronext Securities Oslo, the Norwegian CSD, previously called Euronext VPS. Verdipapirsentralen ASA (VPS) was incorporated in 1985 in connection with the introduction of electronic securities registration to replace physical securities in Norway. Euronext Securities Oslo is the only central securities depository in Norway, and provides an efficient infrastructure and services for the settlement of transactions in securities and the registration of ownership rights over securities. The company offers registration for all the major types of financial instruments that are traded in Norway, namely shares, bonds, equity certificates, short-term bonds and funds. Euronext Securities Oslo is not part of T2S. |

||||||||||

| Bank for International Settlements (BIS) Settlement Model | BIS is an international organisation, which fosters cooperation among central banks and other agencies in pursuit of monetary and financial stability. The Committee on Payments and Market Infrastructures (CPMI) uses three common structural approaches, or models, to categorise the links between delivery and payment in a securities settlement system. |

||||||||||

| Registration Process | Book-Entry: An Act of the Norwegian Parliament related to Euronext Securities Oslo, requires all Oslo Børs listed securities to be registered in the computerised records of the depository. The majority of the most frequently traded, unlisted securities are also registered in the VPS system. The shareholders register maintained by VPS is considered the official registration record. Positions are updated by book-entry movements on settlement date. Transfer of ownership is automatically updated in connection with the transfer of shares in the VPS system. |

||||||||||

| Registrar | The share register is held and updated in the Euronext Securities Oslo. The registrar is a connecting link between the company and Euronext Securities Oslo. |

||||||||||

| Registration Period | The shareholders registry is automatically updated in the Euronext Securities Oslo. |

Risk

| Disclosure Requirements | Shareholdings in this market may be required to be disclosed by the beneficial owner, particularly when such shareholdings reach or exceed prescribed disclosure limits. Investors must ensure that they comply in full by reporting such holdings to the appropriate organisations for this market, within the timeframe required. If you have any questions regarding this issue we encourage you to consult your legal counsel.

Please find attached the rules as stated in the Securities Trading Act section 4-2 and 4-3: |

|---|---|

| Buy-Ins | Allowed by law but is not market practice. |

| Securities Lending | Securities lending is permitted. VPS offers a voluntary lending pool scheme. VPS borrowing is currently restricted to brokers that are members of the Oslo Børs, however, anyone may lend to the pool. |

| Compensation Fund | None |

| Anti-Money Laundering | Norway is a full member of the Financial Action Task Force on Money-Laundering. The Anti-Money Laundering law was altered with effect April 15, 2009 to comply with the new EU directive. The aim is to prevent and reveal transactions in connection with profit from criminal actions or in connection with terrorism. Main duties are to identify clients (KYC) and to report suspicious transactions to The Norwegian National Authority for Investigation and Prosecution of Economic and Environmental Crime (ØKOKRIM). |

Foreign Ownership

| Market Entrance Requirements | For clients serviced out of certain locations this is an FII market. Please refer to the Terms & Conditions for Global Custody or contact your RBC Investor Services' Client Manager before making portfolio investments.

|

|---|---|

| Investment Restrictions | In compliance with EEA-directives regulating banks and insurance companies, certain minimum requirements regarding ownership control have been changed. Any person who intends to acquire a qualified holding in a financial institution must notify this to the competent authorities and obtain prior authorisation. A qualified holding is all holdings representing 10% or more of the capital or the votes in the institution. Further, persons who already hold a qualified holding must apply in advance before acquiring control of more than 20, 25, 33 or 50% of the capital or the votes in the institution. |

| Repatriation Policy | Income, profits and capital can be freely repatriated. |

Cash

| FX Regulations | There are no restrictions on foreign investors FX trading. The Norwegian Krone is fully convertible. In Norway, the NOK can be converted by domestic banks licensed by Norges Bank and branches of foreign credit institutions authorised by a country of the European Union (EU) or the European Economic Area (EEA) to engage in foreign exchange activities. For statistic purposes, domestic banks must report all currency transactions to the Central Bank of Norway. |

|---|---|

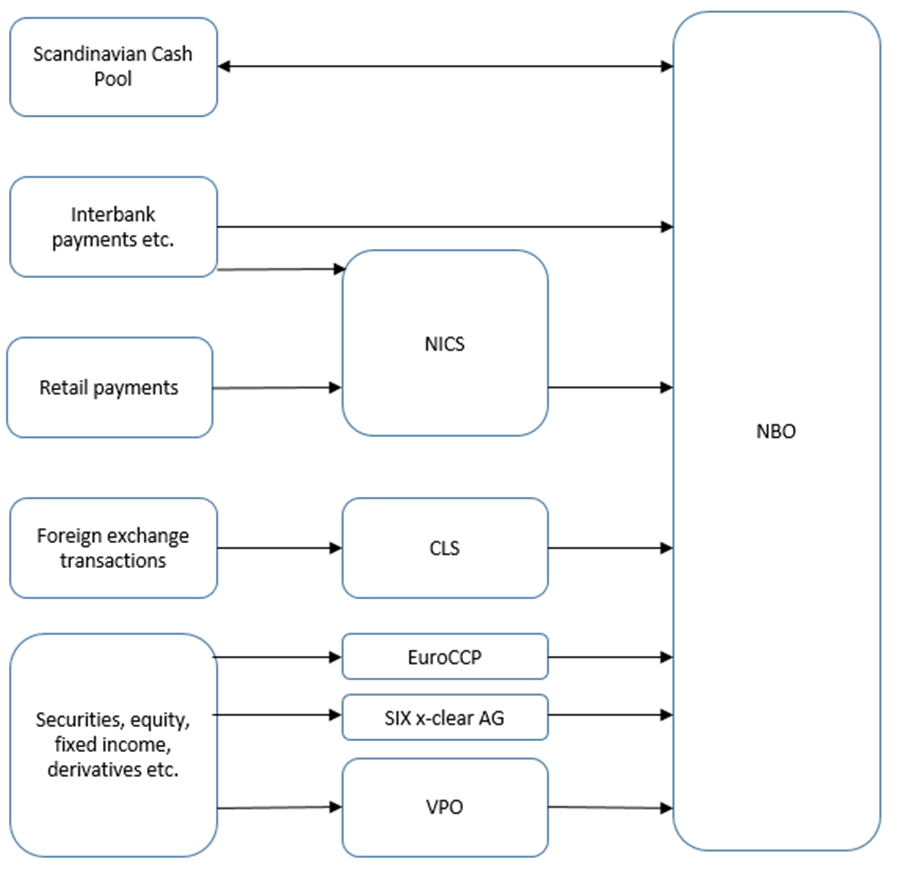

| Payment Systems | The core of the Norwegian NOK payment infrastructure is the Norwegian central bank’s real time gross settlement system (RTGS) called NBO. The system handles high value payments, FX, monetary policy operations connected ancillary systems. However, not all banks hold an account in the NBO system and those who do not link up with a directly connected participant for access to the settlement infrastructure do their settlement through a bank which is a direct participant in NBO.

The connected ancillary systems are: Continuously Linked Settlement (CLS): a multilateral system for FX transactions in presently 18 currencies. Al settlement is done in cycles between 7am – 12pm. Norwegian Interbank Clearing System (NICS) is an interbank payment system that handles both retail payments such as giro, cheques, direct debits and credit transfers. Settlement cycles are at: 05:30am, 09:30am, 11:30am, 1:30pm and 3:30pm. In addition, NICS acts as a routing mechanism for larger payments (from NOK 25 Mill) or express payments, which are routed, to NBO. Scandinavian Cash Pool (SCP) is a collateral management system that allows for cross border intraday liquidity in Denmark, Norway and Sweden. Scandinavian Cash Pool was introduced in 2003. VPO is a securities clearing and settlement system for trades in financial instruments in NOK. The system is part of VPS, the Norwegian central securities depository, part of VPS group. VPO clears and settles transactions from the stock market, fixed income securities etc. EuroCCP and SIX x-clear AG act as central counterparties toward VPO. A new instant payment infrastructure, BRO, which will cover both personal and corporate customers is expected to be launched end of 2018 or early 2019. This project is set on hold as the P27 project will cover BRO requirements. For additional information, please refer to: |

| Overdraft Permitted | Overdrafts are permitted provided that the client has an established credit limit and the overdraft does not exceed the limit. |

{kind=link}

Entitlements

| Dividend Process | Life cycle of dividends:

Foreign registered securities in the VPS may have exceptions to the normal routine of dividend payments. Foreign companies may quote dividends in foreign currency but will pay in NOK. |

||||||

|---|---|---|---|---|---|---|---|

| Dividend Payment Frequency | Norwegian companies usually pay annual dividends. Dividends are normally paid in April-June. Please note that foreign registered companies in the Norwegian market usually pay quarterly dividends. |

||||||

| Interest Payment Frequency | Annual and semi-annual. |

||||||

| Interest Accrual Rate | Interest is calculated based on 360 days. In special cases calculated 365 days. |

||||||

| Corporate Actions |

|

||||||

| Additional Information | Corporate Actions are usually announced well before the effective date, however they must be announced at the latest three banking days after the ex-date. Information sources are the CSD, the Oslo Børs, the issuing companies and the local newspapers. Ex-date in the Norwegian market is the first business day following the last cum-date. Record date is the same date as the calculation date at the CSD, normally 2 days after ex-date. Definition of record date is Ex-date minus 1 plus 3 (normal settlement period). The ex-date is set by the issuing company in the terms and conditions of the issue. |

||||||

| Protection of Rights | Entitlements to rights are determined by the traded stock position at the close of business in the last cum-date and will be calculated on settled positions on record date. Subscription rights are normally credited at record date during the night and confirmed the following morning. The subscription period is set by the company and lasts normally for two weeks, traditionally the same period the subscription rights are traded. Deadline for instructions and to sell or purchase rights is according to notification. |

Proxy Voting

| Foreign Investor Restrictions | Companies are allowed to insert a provision in their articles of association stating that the right to participate and vote at the general meeting can only be exercised if the ownership of shares has been registered in the shareholder register five days prior to the general meeting. Since 1 July 2023 SRD II was implemented in Norway, removing the need to re-register shares to exercise voting rights. |

|---|---|

| Shares Blocked | Shares are not blocked but are re-registered into the name of the beneficial owner, as it is not allowed to vote from nominee accounts. Shares to be voted for cannot be traded, as the beneficial owner would then lose their voting rights. |

| Meeting Notices/Agendas | Provided in English. Extraordinary general meetings must be announced at least 21 days in advance. An "intention to vote" must be received a maximum of five days in advance to facilitate share registration in the name of the beneficial owner. |

| Meeting Outcome | Outcomes of voted resolutions are supplied automatically when votes have been lodged. |

| Company Reports | These are sent directly to all registered shareholders on request. |

| Power of Attorney | Since July 1, 2022, Power of Attorney was no longer required and the below entered into force:

Clients should note that it is possible to vote in Greenlandic and Foroe Islands however a PoA is recommended and require to be dated and shall not be valid for longer than one year from the date of issue. |

| Other | Ordinary shares and "A" shares carry full voting rights; "B" shares carry restricted voting rights. |

Taxation

| Dividend Tax Rate | Foreign Investors are generally subject to 25% withholding tax at source if no tax treaty applies. The normal procedure is to register the correct tax rate in accordance with tax treaty and this is deducted at source. Recent tax reform in Norway will exempt EU Corporate Entities from withholding tax by allowing them to apply for a dividend withholding rate exemption with the tax authorities.

Effective January 1, 2017, standard tax reclaims can be sent for dividends paid up to 5 years (instead of 2 years) earlier. In 2017, standard tax reclaims can be made for dividend payments in 2012 and forward. |

|||

|---|---|---|---|---|

| Interest Tax Rate | Foreign investors are exempt |

|||

| Capital Gains Tax Rate | Foreign investors are exempt |

|||

| Tax Treaties |

|

|||

| Stamp Duty | None |

|||

| Other Taxes | None |

Holiday Calendar

Local Websites

|