Appointed subcustodians

Some markets are restricted for UCITS funds investment – please refer to your depositary team

Denmark

Updated as at December 19, 2023

Market Account Opening Requirements

RBC IS operates an omnibus account structure in this market. For further information or support around accessing this market, please contact your RBC IS representative. Client NoticePlease note not all financial instruments and exchanges listed below are available as an RBCIS product offering. Please consult our Terms & Conditions or reach out to your RBCIS representative for further details. |

Market Statistics

| Currency | Danish Kroner (DKK) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Time Zone | GMT + 1 | ||||||||

| Nasdaq Copenhagen |

July 2021 |

Market Infrastructure

| Exchange(s) | Nasdaq Copenhagen A/S

Approx 132 (as at November 2018) main market listed companies and more than 2,300 bonds, primarily government and mortgage credit bonds, are listed on the exchange. The bond market ranks among the seven largest in Europe in terms of market value. On the market for investment certificates more than 150 are listed. The derivatives market, also called the FUTOP market, is developing positively, but it is small in size by international standards. |

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Trading System | Trading in the following instruments is via Nasdaq Copenhagen's INET trading system:

Derivatives are traded on the Genium Inet trading system. |

||||||||||||

| Trading Hours | Monday to Friday:

|

||||||||||||

| Security Identifiers | ISIN (International Securities Identification Numbering): Used |

||||||||||||

| Regulatory Bodies | The Danish Financial Supervisory Authority (Finanstilsynet) (DFSA) is responsible for the licensing and day-to-day supervision of all entities that play a role in the Danish securities market. As such, the DFSA licenses and supervises, amongst others, banks, stockbrokers, mortgage institutions, insurance companies, investment companies, pension funds, the Nasdaq Copenhagen Stock Exchange and the central securities depository. Its supervisory tasks include the monitoring of the solvency of the banks and the activities of all the above mentioned entities. The DFSA falls under the responsibility of the Ministry of Industry, Business and Financial Affairs. In addition to its supervisory tasks, the DFSA is, in cooperation with the Ministry of Industry, Business and Financial Affairs, also responsible for creating laws regulating the Danish financial sector. In this capacity the DFSA actively participates in the formation of EU legislation. |

||||||||||||

| Instruments |

|

||||||||||||

| Form of Securities | Nearly all listed securities are in book-entry form and generally denominated in DKK. The listed securities cover shares, bonds, money markets instruments, futures, options and mutual funds. |

||||||||||||

| Board Lots |

|

||||||||||||

| Price Variations | In on-exchange trading, the order is to be placed in the trading system and in the market. Equity transactions are executed when the prices of the orders to buy and the orders to sell match or overlap. Best price has priority and orders entered in the order book have priority over orders entered later. A transaction is always executed at the price of the existing order. Danish shares are traded in both round lots and in odd lots, and both are freely tradeable. |

Settlement & Registration

| Settlement Cycles |

|

||||||||

|---|---|---|---|---|---|---|---|---|---|

| Delivery versus Payment (DvP) Settlement Currencies | DKK & EUR |

||||||||

| Over-the-Counter (OTC) | There is limited trading activity in a small over-the-counter market for unlisted securities. |

||||||||

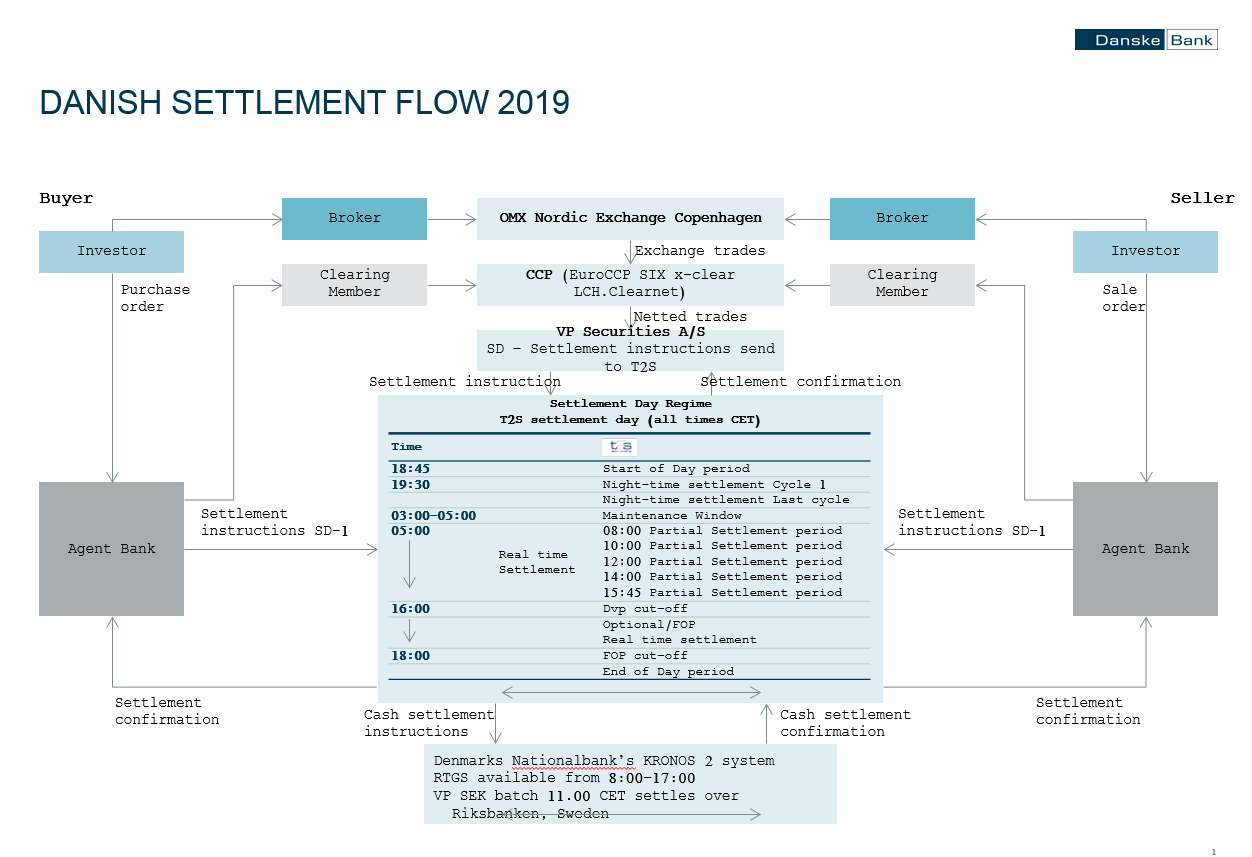

| Settlement Procedures | On-exchange trades are generated automatically from the Nasdaq Copenhagen's trading system via the depository to the sub-custodian's settlement system. No settlement instruction is required. On-exchange trades settle in the same system as off-exchange trades. The local sub-custodian has a fully automated settlement system, which is directly linked to the local CSD, Euronext Securities Copenhagen. When the settlement instruction hits STP requirements, the instruction is forwarded electronically to the CSD with no manual interference. The market employs true delivery versus payment. Free of payment transaction are permitted and T+2 settlement cycle is standard in Denmark, but other settlement cycles are possible. Turnaround trades are permitted and securities lending is allowed to expedite securities settlement. Foreign investors do not need to fund their accounts prior to Settlement Date, but settlement can only take place if there are sufficient funds on the sub-custodian’s account with the central bank. The settlement period in Denmark is T+2. Delivery takes place versus payment, the transfer of securities and funds occurring simultaneously. FOP settlement is also possible.

|

||||||||

| Short Selling | Effective November 1, 2012, the relevant authority must be notified by investors of the short position of shares and government debt when the position reaches or falls below the levels specified in the regulation. The relevant authorities are the local Financial Supervisory Authorities (FSAs). |

||||||||

| Turn-around Trades | As settlement is continuous throughout the settlement day in T2S, same day turnaround trades are possible. Trades can also be linked in T2S, meaning that settlement of a trade is dependent on another trade settling first. |

||||||||

| Clearing Agents | EuroCCP NV (EuroCCP) offers interoperable clearing services for cash equity trades executed on Nasdaq Nordic, and its First North platforms. LCH.Clearnet Ltd offers interoperable clearing services for cash equity trades executed on Nasdaq Nordic, and its First North platforms. SIX x-clear Ltd offers interoperable clearing services for cash equity trades executed on Nasdaq Nordic, and its First North platforms. |

||||||||

| Depositories | Clearing agent and depository are the same legal entity in Denmark. Euronext Securities Copenhagen, the Danish CSD, previously called VP Securities is the only depository in Denmark. |

||||||||

| Bank for International Settlements (BIS) Settlement Model | BIS is an international organisation which fosters cooperation among central banks and other agencies in pursuit of monetary and financial stability. The Committee on Payments and Market Infrastructures (CPMI) uses three common structural approaches, or models, to categorise the links between delivery and payment in a securities settlement system. |

||||||||

| Registration Process | Book-Entry: |

||||||||

| Registrar | There is no central registrar and issuers very often appoint agents as registrars. |

||||||||

| Registration Period | Registration of dematerialised securities takes place automatically upon settlement. Automatic registration is an integrated part of the processing of a securities transfer and it is initiated by VP. Physical share certificates are initially issued as registered but they assume bearer identity after the first delivery. The re-registration of physical shares is done by the company itself upon request by the owner of the shares. Registration period for physical securities/proxy – There are no specific rules on how registration on physical securities should be. The rules are depended on the company’s regulations. |

Risk

| Disclosure Requirements | Registration of dematerialised securities takes place automatically upon settlement. Automatic registration is an integrated part of the processing of a securities transfer and it is initiated by VP. Physical share certificates are initially issued as registered but they assume bearer identity after the first delivery. The re-registration of physical shares is done by the company itself upon request by the owner of the shares. |

|---|---|

| Buy-Ins | Nasdaq Copenhagen's Buy-in process: Only relevant for On Exchange and CCP trades In addition late settlement fees are applied with two cost elements for the failing delivery party; a fixed fee and a variable cost: The fixed fee for the failing party is €25 per day per failing settlement position. The variable cost of 100bp per annum charged on a daily basis for the value of the failing settlement position was discontinued on February 1, 2014. |

| Securities Lending | Securities lending is legally permitted in Denmark. It is practised and there are established rules for the implementation of such transactions and for the collateral required. There is no centralised stock lending facilities with the CSD or the Exchange - Lending is available via commercial bank programmes |

| Compensation Fund | The CSD and the Stock Exchange have insurance which covers loss due to negligence, fraud and default. |

| Anti-Money Laundering | Denmark is one of the charter members of the Financial Action Task Force on Money Laundering (FATF) and, as a member of the European Union (when applicable), is subject to the EU regulations concerning anti money laundering and the prevention of terrorist financing. |

Foreign Ownership

| Market Entrance Requirements | Denmark is an FII market for the purposes of proxy voting only. Please contact your RBC Investor Services' Client Manager. There are no market entry requirements specific to foreign investors. |

|---|---|

| Investment Restrictions | None |

| Repatriation Policy | Funds can be repatriated freely. |

Cash

| FX Regulations | No specific regulations. |

|---|---|

| Payment Systems | The Danish Central Bank, Denmark's National Bank, plays a key role in relation to settlement of payments between banks and most payments are effected via the banks' accounts with Denmark's National Bank. The Denmark National Bank participates in the European payment system. Sum Clearing Intraday Clearing Straksclearing VP Settlement Clearing I Kronos 2 VP Settlement Clearing I T2S Settlement can only take place if there are sufficient funds on the bank's account with Denmark's National Bank. |

| Overdraft Permitted | No specific regulations. This is negotiated bilaterally between the parties. |

Entitlements

| Dividend Process | Dividends are declared at companies' Annual General Meeting (AGM). The Danish Companies Act was amended on July 1, 2004 making the payment of extraordinary dividends permissible. Some unit trust funds investing in bonds pay interim dividends. Alternatives to cash dividends, such as stock dividends or reinvestment plans, are rare. When submitting a claim for refund of dividend tax, the following must be submitted along with the claim: SUPPLEMENTARY DOCUMENTATION

|

|---|---|

| Dividend Payment Frequency | Annually, on the third business day following the annual general meeting. However, payments of additional dividends are possible. |

| Interest Payment Frequency | Interest on most government bonds is paid annually, whereas interest on mortgage bonds is paid annually, semi-annually or quarterly. |

| Interest Accrual Rate | Actual/actual basis. |

| Corporate Actions | Common Events: Bonus and subscription rights, mergers, tenders and stock splits. |

| Additional Information | All corporate events are processed through VP Securities A/S, the Danish Central Depository. |

| Protection of Rights | According to Danish law, to exercise voting rights, a shareholder must either attend a general meeting in person or exercise them by proxy. Information regarding SRD2 - Issuers of shares who have their home office in an EU Member State, and whose securities are traded on the EU/EEA’s regulated markets, need to comply with the requirements outlined in the directive. SRDII establishes rights that enable Issuers to identify their shareholders, informs shareholders proactively and creates a framework for shareholders to have easier access to exercise of their shareholder rights. For example, by voting at general meetings. SRDII gives issuers the right to identify all their shareholders. All intermediaries who hold the share in question, either on their own account or on account on behalf of someone else, are required to respond to the Issuer’s request. The Issuer has the right to appoint an intermediary to collect the shareholder information from other intermediaries in the chain. |

Proxy Voting

| Foreign Investor Restrictions | RBC Investor Services' sub-custodian offers proxy voting services for all clients who hold shares in segregated accounts and in nominee accounts. |

|---|---|

| Shares Blocked | No |

| Meeting Notices/Agendas | The date for an upcoming General Meeting (GM) must be published at least eight weeks prior to the date of the meeting. Shareholders have the right to request that items are added to the GM agenda. Official meeting notice including agenda must be announced between five to three weeks prior to the meeting. |

| Meeting Outcome | The minutes including the specifications of voting for each proposal must be published within two weeks of the meeting. |

| Company Reports | Provided on best effort basis. Reports are available in English from major companies, usually on the company website. |

| Power of Attorney | Noo longer required in Denmark. However if you want to vote for Greenland and Faroe Island it is required to provide a PoA. |

| Other | Record/registration date of seven calendar days before the meeting. |

Taxation

| Dividend Tax Rate | 27% withholding tax. The reclaimable amount following from a Double Taxation Treaty must be reclaimed, as there is very limited relief at source in Denmark for clients other than those named below. Danish companies, which have segregated custody accounts registered in the beneficial owner's name at VP, are eligible for tax relief at source of 25%. These companies do not have to reclaim tax after dividend payments. Due to the discovery of extensive fraud in the Danish reclaim process up to and in 2015, the Danish Tax Authorities introduced a new, electronic reclaim procedure, replacing both reclaims via physical forms and via the electronic block reclaims, where minimal information was required. There is now only one method to reclaim, starting 1st April 2017. DANISH DIVIDEND TAX RECLAIM PROCEDURE FROM 1ST APRIL 2017 A reclaim spreadsheet detailing the basis for the reclaim must be forwarded to the local sub-custodian together with the relevant supplementary documents in pdf form. SUPPLEMENTARY DOCUMENTATION REQUIRED FROM RBC’S CLIENT

Templates for the below two documents are available on the Tax Authorities website at: http://www.skat.dk/SKAT.aspx?oId=2236538&vId=0&lang=US

Template for the below document is available on the Tax Authorities website at: http://www.skat.dk/skat.aspx?oId=119350

The local sub-custodian will liaise with the Danish Tax Authorities, ensuring that all necessary information has been supplied. When the reclaim has been fully processed, the amount will be credited your cash account. The Danish tax authorities announced that the Statute of Limitations for the reclaim of Danish dividend tax based on Double Taxation treaties was reduced from 5 to 3 years as of 13th September 2016 The Danish withholding tax on Danish dividends received by non-resident companies was reduced from 27% to 22% as of July 1, 2016. The reduction to 22% also benefits companies from outside the EU/EAA area for dividends received after July 1, 2016. As Danish legislation is considered to have been in conflict with EU legislation, companies resident in the EU/EEA states, which have paid higher tax rates than that applicable for Danish companies, may reclaim excess withheld tax as follows:

This amendment has no impact for individuals, the withholding tax remains at 27% for individuals. As of March 1, 2023, a full tax exemption via domestic law will no longer be available to beneficial owners qualifying as foreign states (and their institutions). Beneficial owners that are residents of a Double Taxation Treaty (DTT) country may however reclaim withholding tax on dividends using the standard refund procedure. |

||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Interest Tax Rate | Exempt |

||||||||||||||||||||||||||||||||

| Capital Gains Tax Rate | Exempt |

||||||||||||||||||||||||||||||||

| Tax Treaties |

Treaties with France and Spain: following the termination of the double taxation treaties with France and Spain on January 1, 2009, the Danish tax authorities decided to allow tax reclaims from both Spanish and French investors. |

||||||||||||||||||||||||||||||||

| Stamp Duty | No stamp duty is paid in the Danish market. |

||||||||||||||||||||||||||||||||

| Other Taxes | None |

Holiday Calendar

Local Websites

|